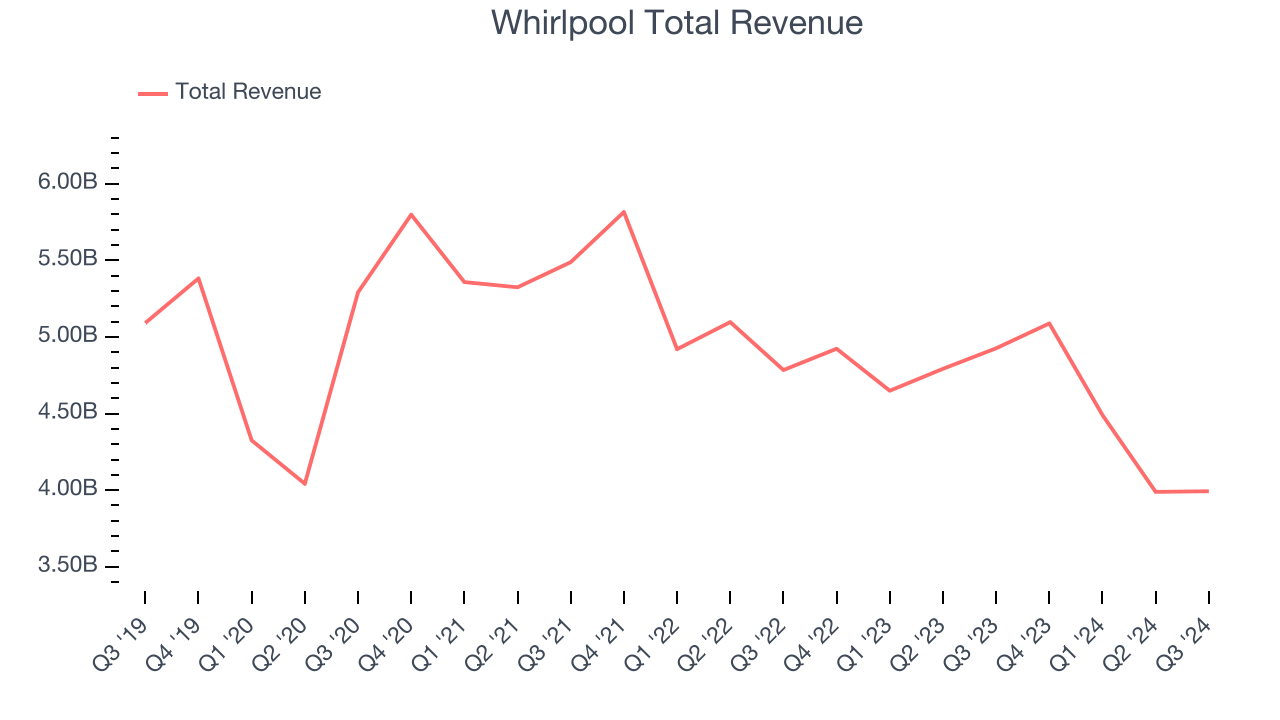

Home appliances manufacturer Whirlpool (NYSE:WHR) missed Wall Street’s revenue expectations in Q3 CY2024, with sales falling 18.9% year on year to $3.99 billion. On the other hand, the company’s outlook for the full year was close to analysts’ estimates with revenue guided to $16.9 billion at the midpoint. Its GAAP profit of $2 per share was also 18.2% below analysts’ consensus estimates.

Is now the time to buy Whirlpool? Find out by accessing our full research report, it’s free.

Whirlpool (WHR) Q3 CY2024 Highlights:

- Revenue: $3.99 billion vs analyst estimates of $4.09 billion (2.4% miss)

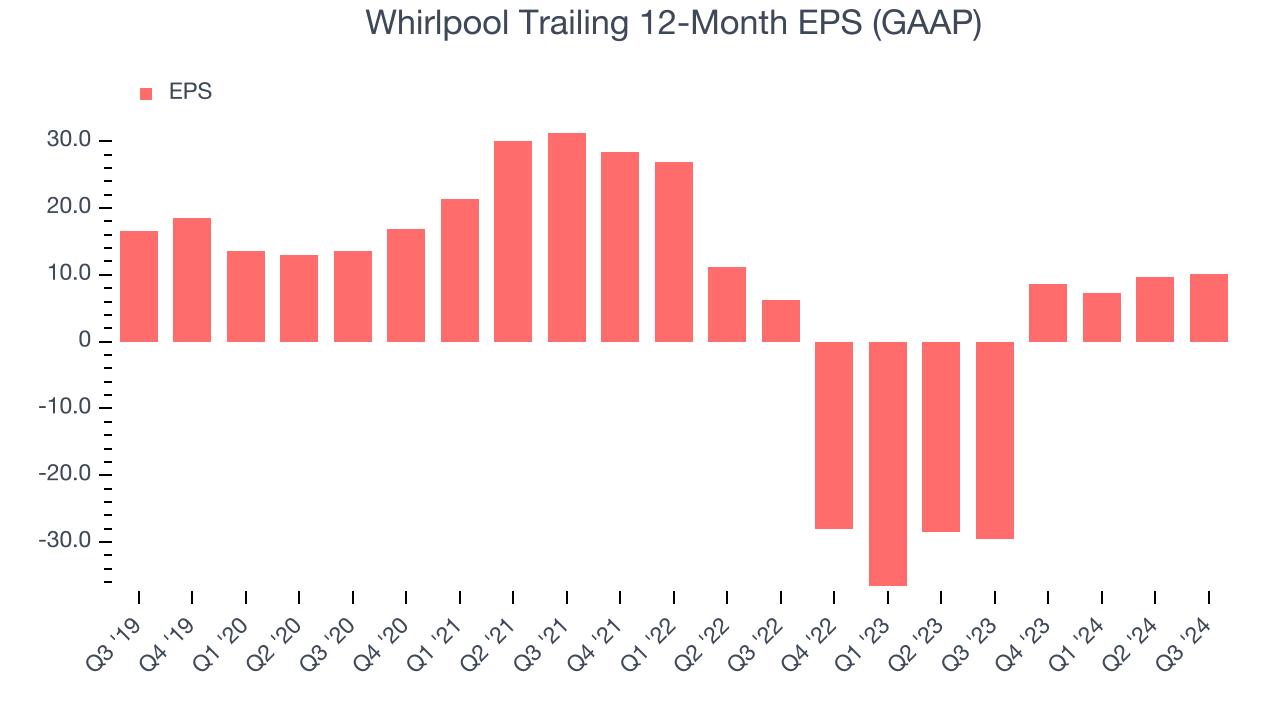

- EPS: $2 vs analyst expectations of $2.45 (18.2% miss)

- EBITDA: $344 million vs analyst estimates of $347.3 million (small miss)

- The company reconfirmed its revenue guidance for the full year of $16.9 billion at the midpoint

- EPS (GAAP) guidance for the full year is $0.50 at the midpoint, missing analyst estimates by 89.8%

- Gross Margin (GAAP): 16.1%, in line with the same quarter last year

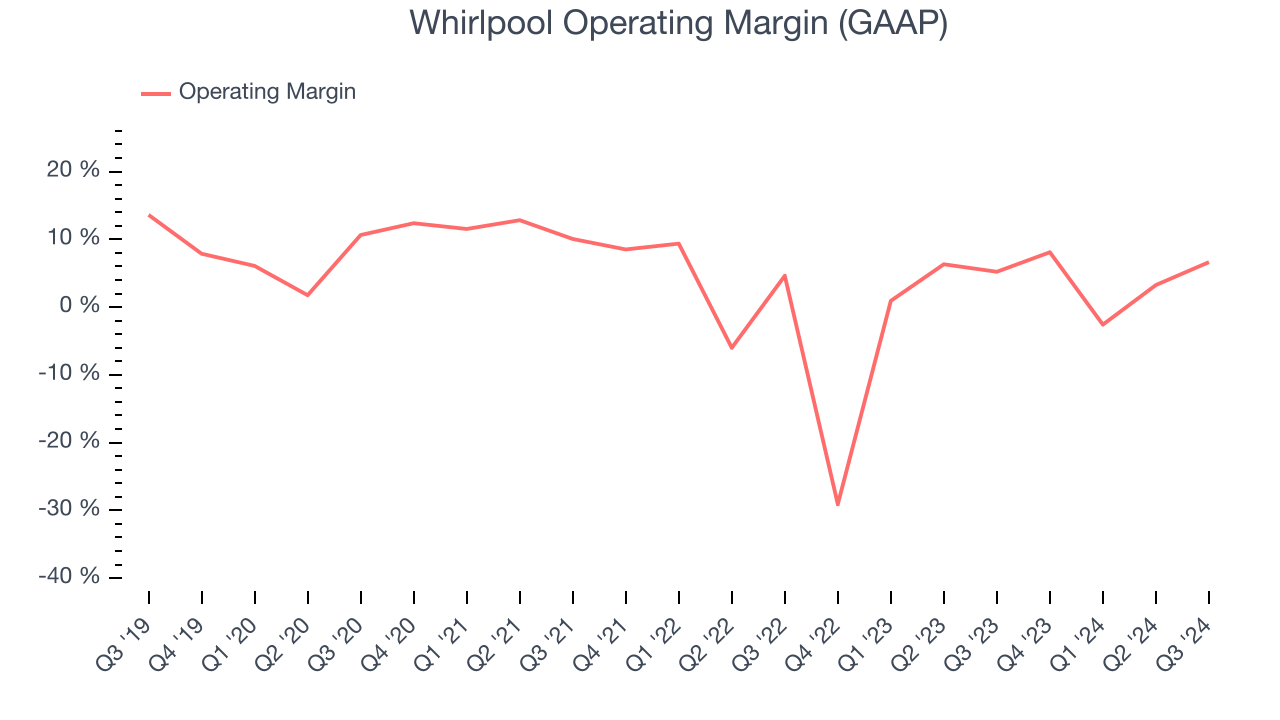

- Operating Margin: 6.6%, up from 5.2% in the same quarter last year

- EBITDA Margin: 8.6%, up from 6.9% in the same quarter last year

- Free Cash Flow was $127 million, up from -$73 million in the same quarter last year

- Market Capitalization: $5.62 billion

"In Q3, we continued to deliver sequential ongoing EBIT margin expansion despite the unfavorable macroeconomic environment we are experiencing in North America," said Marc Bitzer.

Company Overview

Credited with introducing the first automatic washing machine, Whirlpool (NYSE:WHR) is a manufacturer of a variety of home appliances.

Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Sales Growth

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Whirlpool’s revenue declined by 3.2% per year. This shows demand was weak, a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Whirlpool’s recent history shows its demand has stayed suppressed as its revenue has declined by 7.7% annually over the last two years. Whirlpool isn’t alone in its struggles as the Electrical Systems industry experienced a cyclical downturn, with many similar businesses seeing lower sales at this time.

This quarter, Whirlpool missed Wall Street’s estimates and reported a rather uninspiring 18.9% year-on-year revenue decline, generating $3.99 billion of revenue.

Looking ahead, sell-side analysts expect revenue to decline 8.4% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and illustrates the market believes its newer products and services will not catalyze better top-line performance yet.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

Whirlpool was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.7% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Whirlpool’s annual operating margin decreased by 3 percentage points over the last five years. The company’s performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn’t pass those costs onto its customers.

In Q3, Whirlpool generated an operating profit margin of 6.6%, up 1.4 percentage points year on year. The increase was encouraging, and since its operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as marketing, R&D, and administrative overhead.

Earnings Per Share

Analyzing long-term revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Whirlpool, its EPS by declined more than its revenue over the last five years, dropping 9.3% annually. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Diving into the nuances of Whirlpool’s earnings can give us a better understanding of its performance. As we mentioned earlier, Whirlpool’s operating margin improved this quarter but declined by 3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business. For Whirlpool, its two-year annual EPS growth of 28% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q3, Whirlpool reported EPS at $2, up from $1.50 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Whirlpool’s full-year EPS of $10.16 to grow by 10.9%.

Key Takeaways from Whirlpool’s Q3 Results

It was good to see Whirlpool’s full-year revenue forecast beat analysts’ expectations. On the other hand, its full-year EPS outlook missed due to a non-cash charge related to an acquisition it made earlier in the year. Overall, this was a weaker quarter, but the stock traded up 3.2% to $102.50 immediately after reporting. This was likely due to the better-than-anticipated revenue guidance.

So should you invest in Whirlpool right now?We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.