Qualcomm has gotten torched over the last six months - since May 2024, its stock price has dropped 24.2% to $157.89 per share. This might have investors contemplating their next move.

Given the weaker price action, is now a good time to buy QCOM? Find out in our full research report, it’s free.

Why Does Qualcomm Spark Debate?

Having been at the forefront of developing the standards for cellular connectivity for over four decades, Qualcomm (NASDAQ:QCOM) is a leading innovator and a fabless manufacturer of wireless technology chips used in smartphones, autos and internet of things appliances.

Two Positive Attributes:

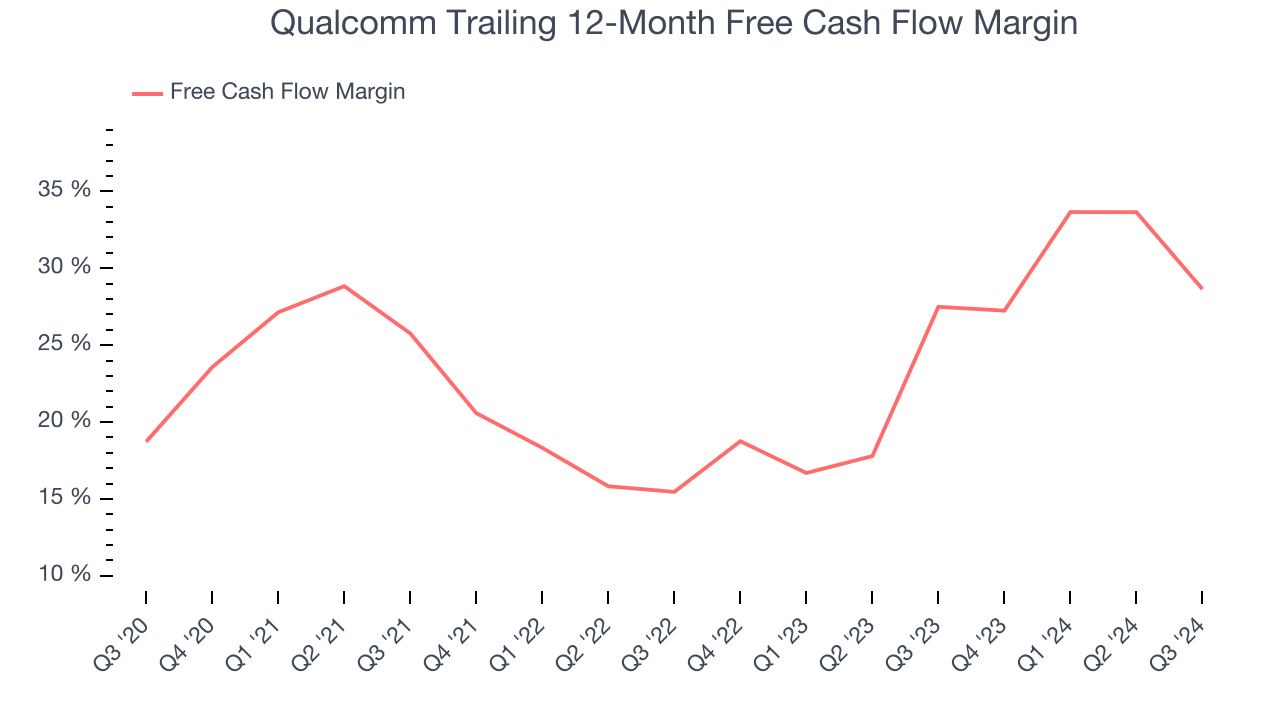

1. Increasing Free Cash Flow Margin Juices Financials

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Qualcomm’s margin expanded by 9.9 percentage points over the last five years. This shows the company is heading in the right direction, and because its free cash flow profitability rose more than its operating profitability, continued increases could suggest it’s becoming a less capital-intensive business. Its free cash flow margin for the trailing 12 months was 28.6%.

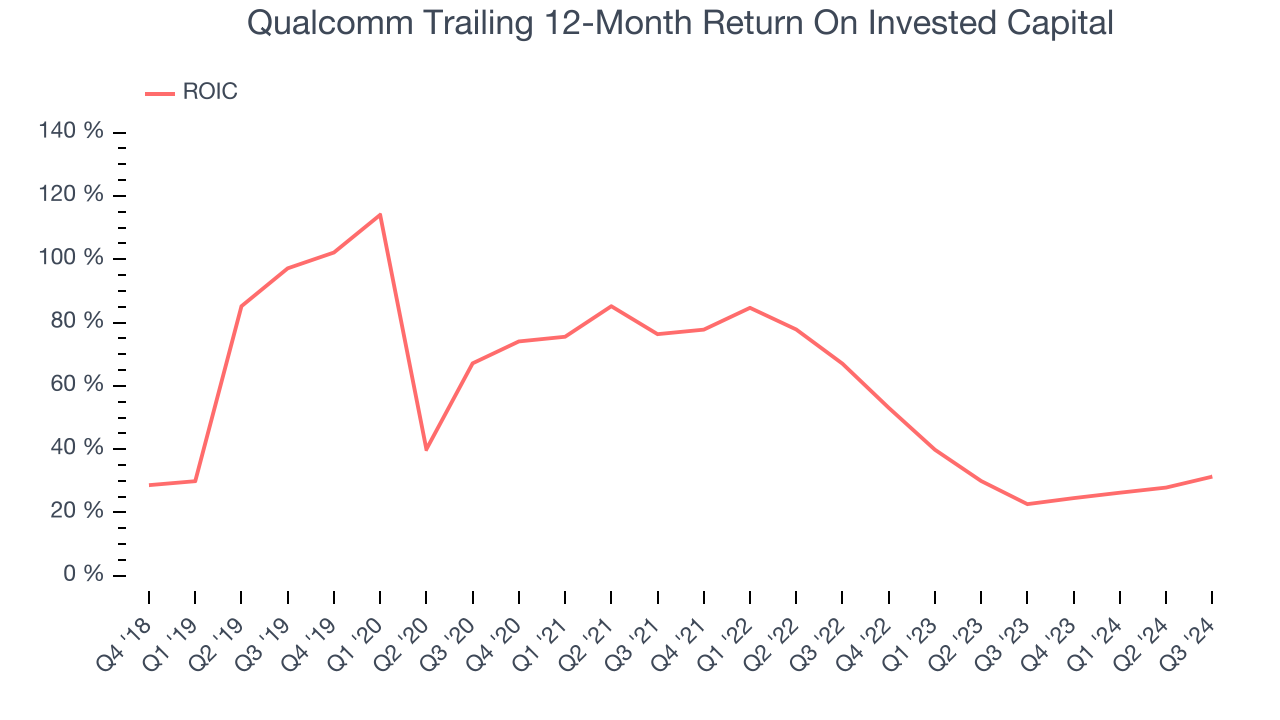

2. Stellar ROIC Showcases Lucrative Growth Opportunities

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Qualcomm’s five-year average ROIC was 52.9%, placing it among the best semiconductor companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

One Reason to be Careful:

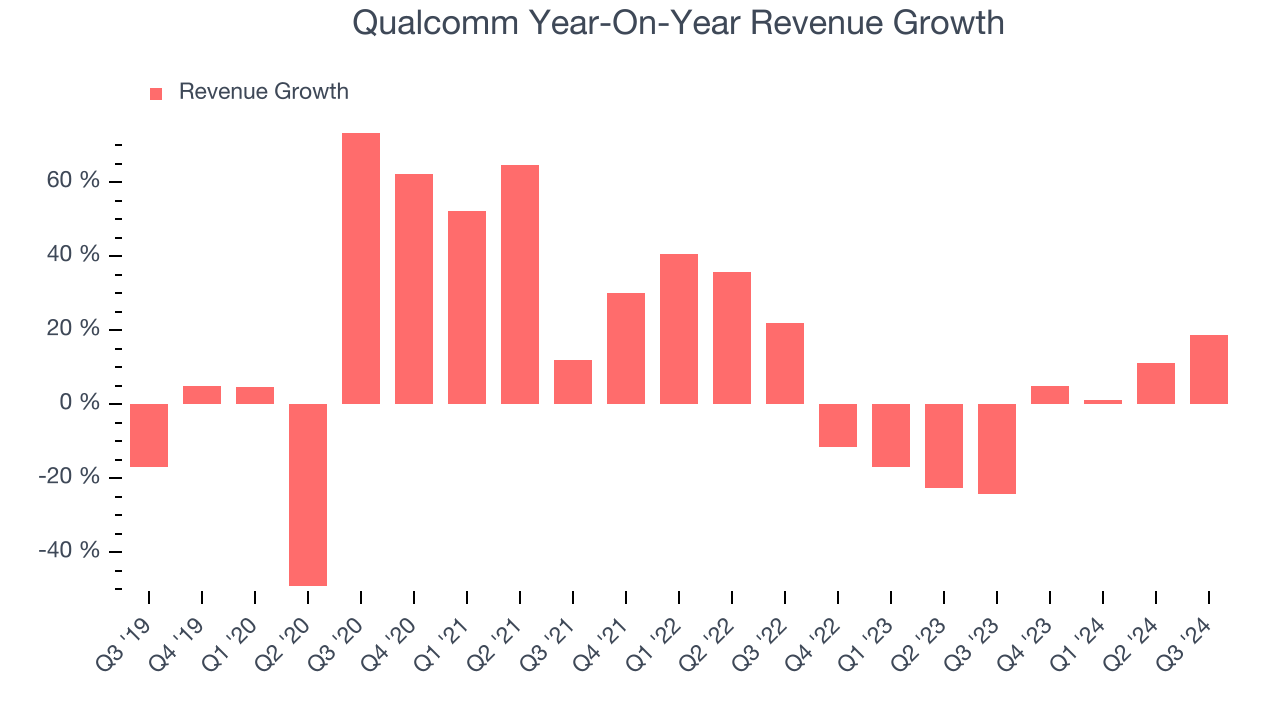

Revenue Tumbling Downwards

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Qualcomm’s recent history marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 6.1% over the last two years.

Final Judgment

Qualcomm’s positive characteristics outweigh the negatives. With the recent decline, the stock trades at 14x forward price-to-earnings (or $157.89 per share). Is now the right time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Qualcomm

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.