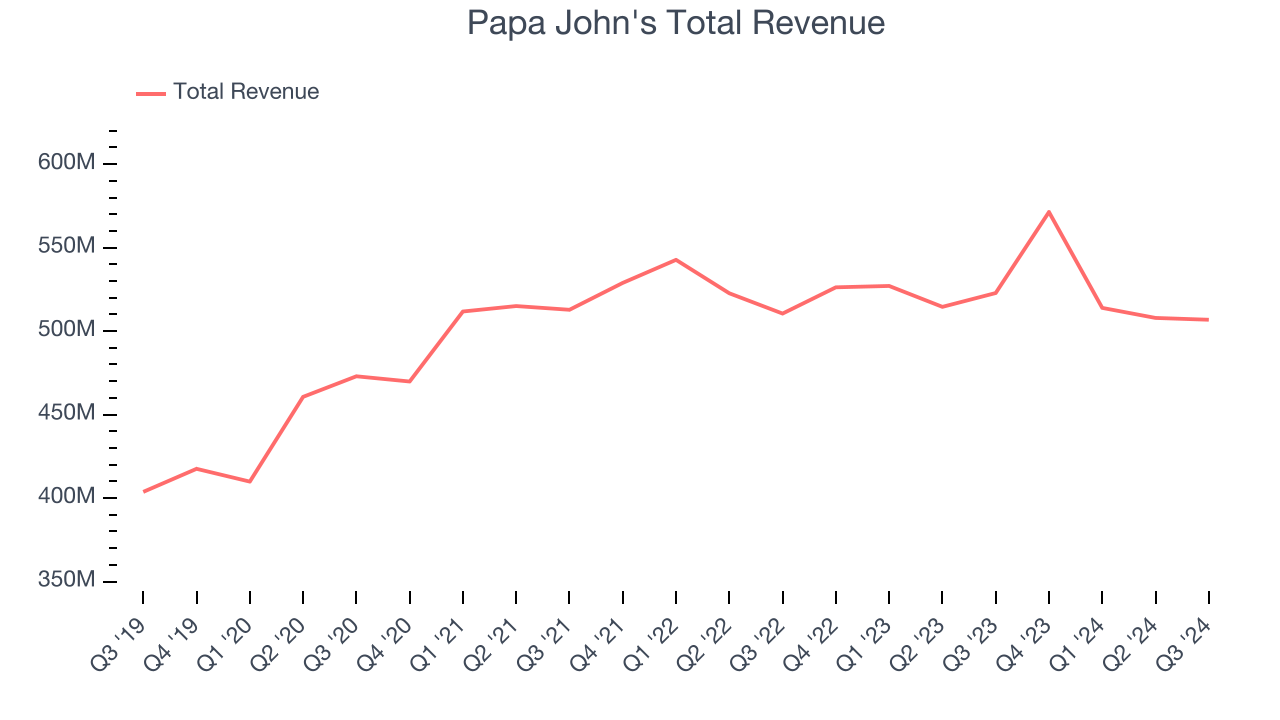

Fast-food pizza chain Papa John’s (NASDAQ:PZZA) reported Q3 CY2024 results topping the market’s revenue expectations, but sales fell 3.1% year on year to $506.8 million. Its non-GAAP profit of $0.43 per share was in line with analysts’ consensus estimates.

Is now the time to buy Papa John's? Find out by accessing our full research report, it’s free.

Papa John's (PZZA) Q3 CY2024 Highlights:

- Revenue: $506.8 million vs analyst estimates of $498.6 million (1.6% beat)

- Adjusted EPS: $0.43 vs analyst expectations of $0.43 (in line)

- Gross Margin (GAAP): 29.9%, in line with the same quarter last year

- Operating Margin: 12.9%, up from 6.1% in the same quarter last year

- Free Cash Flow Margin: 1.8%, down from 3.3% in the same quarter last year

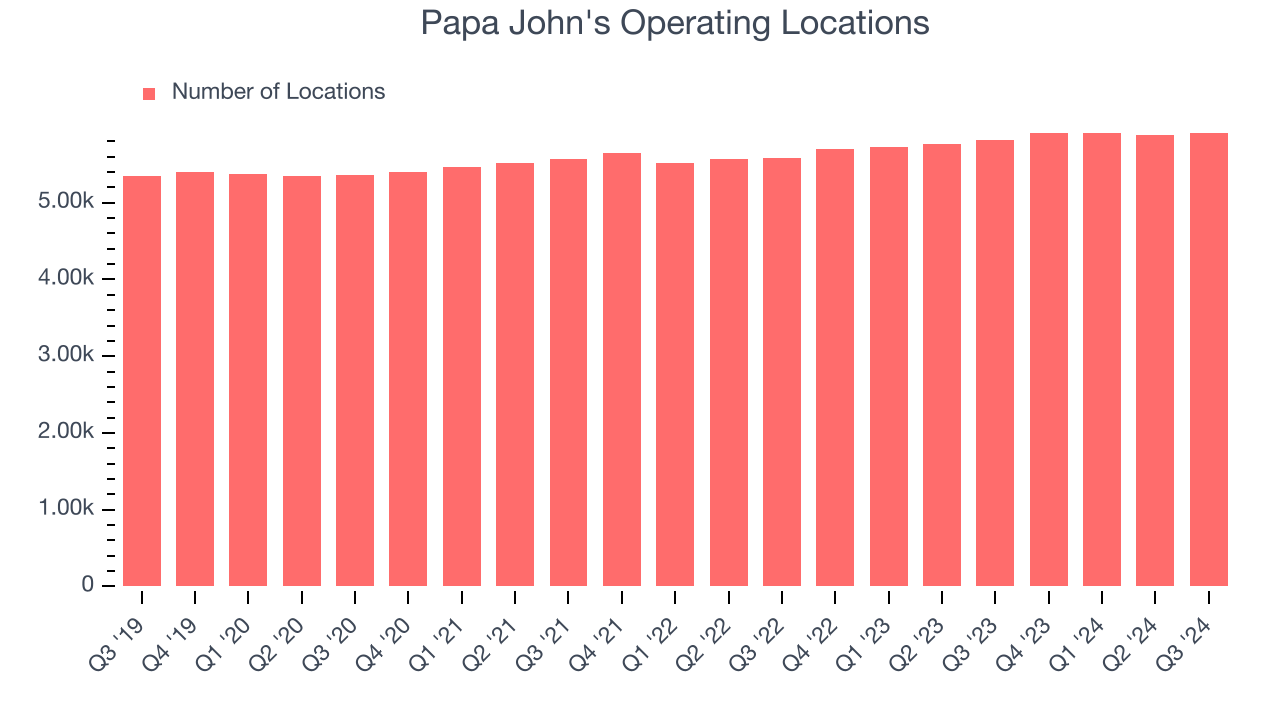

- Locations: 5,908 at quarter end, up from 5,817 in the same quarter last year

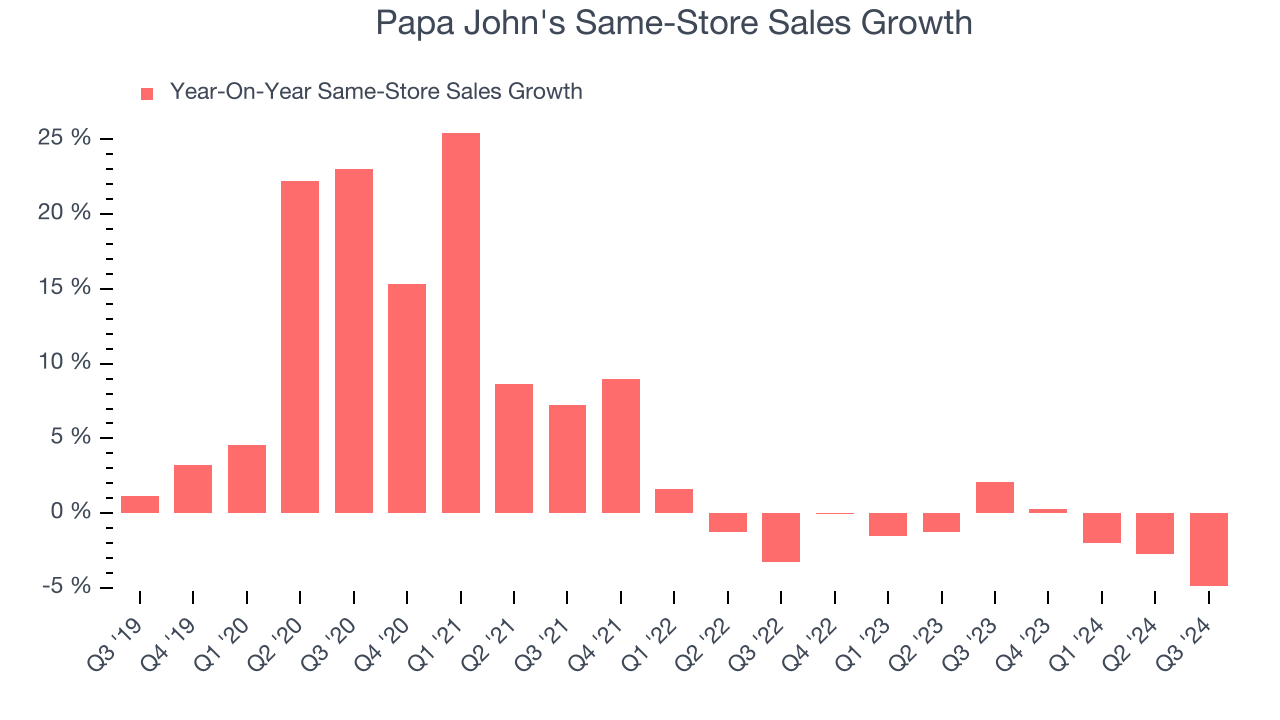

- Same-Store Sales fell 4.9% year on year (2.1% in the same quarter last year)

- Market Capitalization: $1.90 billion

Company Overview

Founded by the eclectic John “Papa John” Schnatter, Papa John’s (NASDAQ:PZZA) is a globally recognized pizza delivery and carryout chain known for “better ingredients” and “better pizza”.

Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Sales Growth

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years.

Papa John's is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Papa John’s sales grew at a tepid 5.6% compounded annual growth rate over the last five years (we compare to 2019 to normalize for COVID-19 impacts).

This quarter, Papa John’s revenue fell 3.1% year on year to $506.8 million but beat Wall Street’s estimates by 1.6%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last five years. This projection is underwhelming and illustrates the market believes its offerings will face some demand challenges.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Restaurant Performance

Number of Restaurants

Papa John's operated 5,908 locations in the latest quarter. It has opened new restaurants quickly over the last two years and averaged 2.8% annual growth, faster than the broader restaurant sector. Furthermore, one dynamic making expansion more seamless is the company’s franchise model, where franchisees are primarily responsible for opening new restaurants while Papa John's provides support.

When a chain opens new restaurants, it usually means it’s investing for growth because there’s healthy demand for its meals and there are markets where the concept has few or no locations.

Same-Store Sales

The change in a company's restaurant base only tells one side of the story. The other is the performance of its existing locations, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing restaurants and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Papa John’s demand has been shrinking over the last two years as its same-store sales have averaged 1.3% annual declines. This performance is concerning - it shows Papa John's artificially boosts its revenue by building new restaurants. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its restaurant base.

In the latest quarter, Papa John’s same-store sales fell by 4.9% annually. This decline was a reversal from the 2.1% year-on-year increase it posted 12 months ago. We’ll keep a close eye on the company to see if this turns into a longer-term trend.

Key Takeaways from Papa John’s Q3 Results

We like that Papa John's revenue outperformed Wall Street’s estimates on better same-store sales. Holding aside expectations, same-store sales still declined a pretty meaningful amount, which is never good. The market seemed to focus on the negatives, and the stock traded down 1.5% to $57.37 immediately after reporting.

So do we think Papa John's is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.