Armstrong World has had an impressive run over the past six months as its shares have beaten the S&P 500 by 24.8%. The stock now trades at $157.08, marking a 36.9% gain. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Armstrong World, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons why there are better opportunities than AWI and a stock we'd rather own.

Why Is Armstrong World Not Exciting?

Started as a two-man shop dating back to the 1860s, Armstrong (NYSE:AWI) provides ceiling and wall products to commercial and residential spaces.

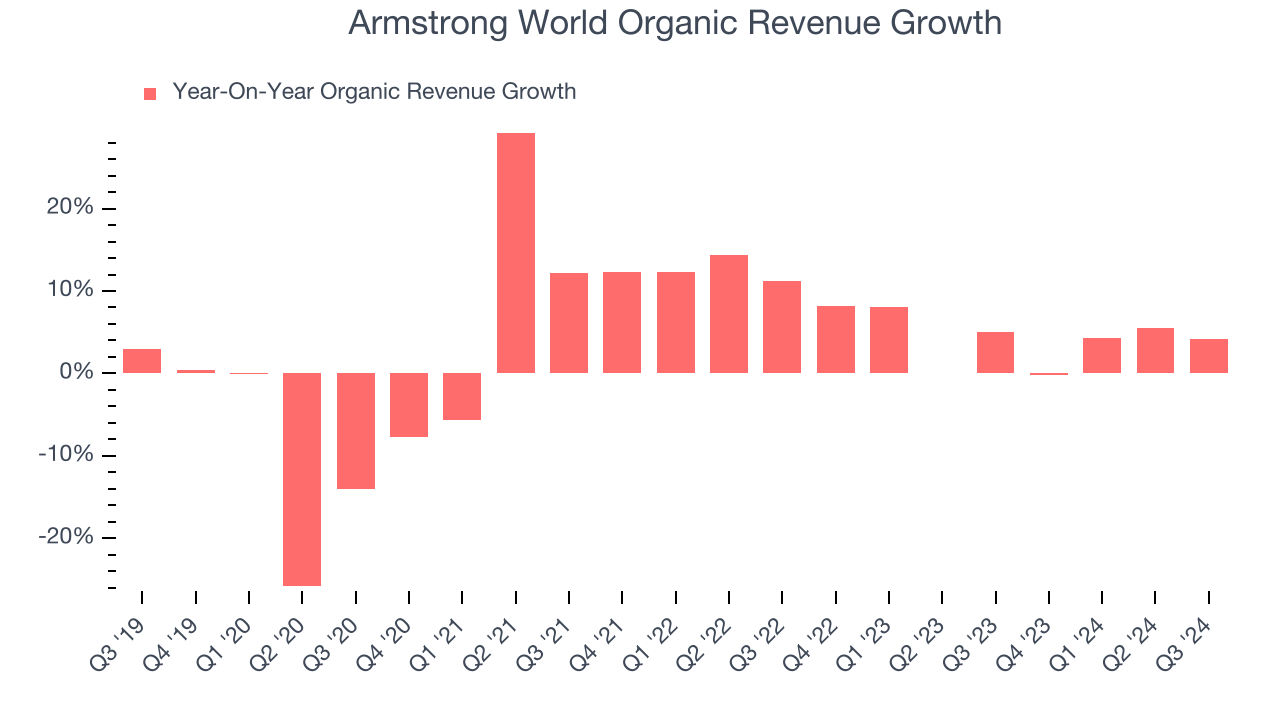

1. Slow Organic Growth Suggests Waning Demand In Core Business

In addition to reported revenue, organic revenue is a useful data point for analyzing Building Materials companies. This metric gives visibility into Armstrong World’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Armstrong World’s organic revenue averaged 4.4% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

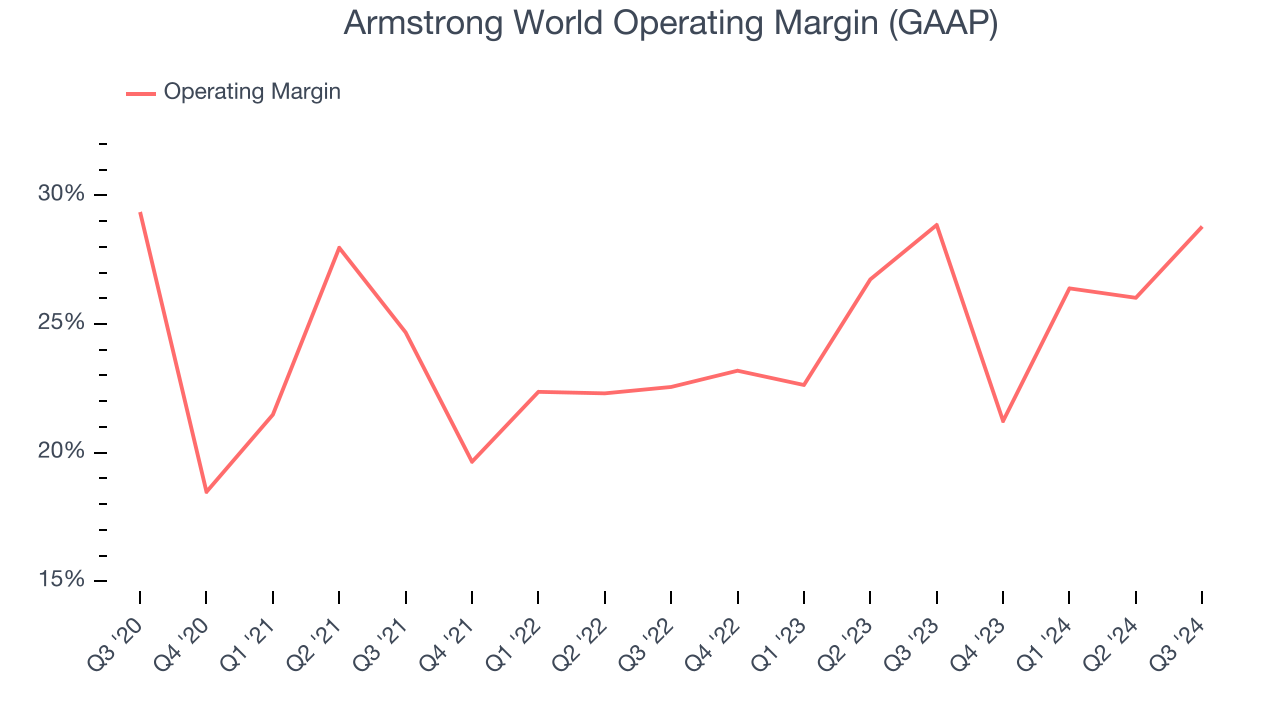

2. Operating Margin Falling

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Looking at the trend in its profitability, Armstrong World’s operating margin decreased by 3.1 percentage points over the last five years. Even though its historical margin is high, shareholders will want to see Armstrong World become more profitable in the future. Its operating margin for the trailing 12 months was 25.8%.

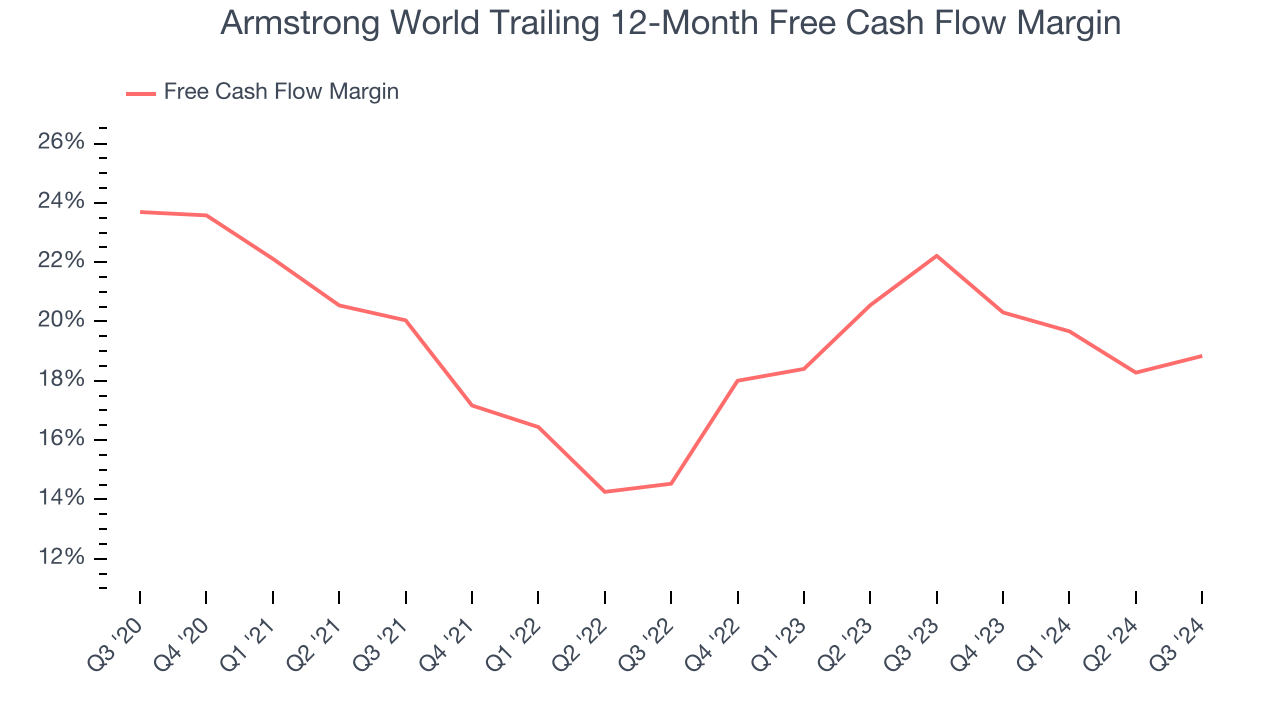

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Armstrong World’s margin dropped by 4.9 percentage points over the last five years. If its declines continue, it could signal higher capital intensity. Armstrong World’s free cash flow margin for the trailing 12 months was 18.8%.

Final Judgment

Armstrong World’s business quality ultimately falls short of our standards. With its shares topping the market in recent months, the stock trades at 23.7× forward price-to-earnings (or $157.08 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. We’d suggest looking at Wabtec, a leading provider of locomotive services benefiting from an upgrade cycle.

Stocks We Like More Than Armstrong World

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.