EVERETT, Wash., Oct. 28, 2024 (GLOBE NEWSWIRE) -- Coastal Financial Corporation (Nasdaq: CCB) (the “Company”, "Coastal", "we", "our", or "us"), the holding company for Coastal Community Bank (the “Bank”), through which it operates a community-focused bank with an industry leading banking as a service ("BaaS") segment, today reported unaudited financial results for the quarter ended September 30, 2024, including net income of $13.5 million, or $0.97 per diluted common share, compared to $11.6 million, or $0.84 per diluted common share, for the three months ended June 30, 2024.

Management Discussion of the Quarter

“The third quarter demonstrated strong momentum across both our community bank and CCBX operating segments, despite a still challenging operating environment,” said CEO Eric Sprink. “We saw high quality net loan growth of $92.4 million despite selling $423.7 million in loans. We are implementing strategies to increase fee income and we continue to build out and invest in an infrastructure that is scalable, and that we believe will enable us to be innovative leaders in financial services.”

Key Points for Third Quarter and Our Go-Forward Strategy

- Balance Sheet Well Positioned for Lower Rates. Our balance sheet stands in a modestly liability sensitive position as of September 30, 2024, with $1.95 billion of CCBX deposits that contractually reprice lower immediately upon any reduction in the Federal Funds Rate, with $1.09 billion of CCBX loans repricing in 90 days or less following such reduction. The Federal Open Market Committee recently lowered the targeted Federal Funds rate 0.50% on September 19, 2024; a reduction of 0.50% compared to June 30, 2024 and September 30, 2023. The rate decrease came late in the quarter, so the full impact of this and any subsequent rate changes will be reflected in future periods.

- Expanding Relationships with CCBX Partners. We continue to focus on expanding product offerings with existing CCBX partners. We believe that launching new products with existing partners positions us to reach a wide and established customer base with modest increase in enterprise risk. Products launched in 2024 with existing partners have gained traction and are growing the balance sheet and increasing income. The pipeline for CCBX is active, although we expect to remain selective in adding new partners to manage risk and capital.

- On-going Loan Sales. We sold $423.7 million loans in the quarter ended September 30, 2024 as part of our strategy to balance credit risk, manage partner and lending limits, protect capital levels and move credit card balances to an off balance sheet fee generating model. We are retaining a portion of the fee income for our role in processing transactions on sold credit card balances. This provides an on-going and passive revenue stream with no on balance sheet risk.

- Continued Regulatory and Compliance Infrastructure Investments Position Us Well for Next Phase of Growth. We continue to utilize co-sourced personnel as a component of our risk and compliance efforts. This flexible co-sourcing approach allows us to manage the growth of our internal team while also ensuring CCBX has the resources it needs. While we remain 100% indemnified against partner fraud losses, we were encouraged to see fraudulent activity amongst our partners remains low during the current quarter, compared to the same period last year, a positive indicator of our continued investments in our risk infrastructure.

- Reorganization and Strengthening of Talent to Accommodate Growth and Plans for the Future. We recently announced the bifurcation of the President of the Bank into two roles, appointing Brian Hamilton as President of CCBX, the Fintech and BaaS segment of the Bank, with Curt Queyrouze serving as President of the community bank and corporate credit.

Third Quarter 2024 Financial Highlights

The tables below outline some of our key operating metrics.

| Three Months Ended | ||||||||||||||||||||

| (Dollars in thousands, except share and per share data; unaudited) | September 30, 2024 | June 30, 2024 | March 31, 2024 | December 31, 2023 | September 30, 2023 | |||||||||||||||

| Income Statement Data: | ||||||||||||||||||||

| Interest and dividend income | $ | 105,079 | $ | 97,487 | $ | 90,472 | $ | 88,243 | $ | 88,331 | ||||||||||

| Interest expense | 32,892 | 31,250 | 29,536 | 28,586 | 26,102 | |||||||||||||||

| Net interest income | 72,187 | 66,237 | 60,936 | 59,657 | 62,229 | |||||||||||||||

| Provision for credit losses | 70,257 | 62,325 | 83,158 | 60,789 | 27,253 | |||||||||||||||

| Net interest (expense)/ income after provision for credit losses | 1,930 | 3,912 | (22,222 | ) | (1,132 | ) | 34,976 | |||||||||||||

| Noninterest income | 80,068 | 69,918 | 86,955 | 64,694 | 34,579 | |||||||||||||||

| Noninterest expense | 65,616 | 58,809 | 56,018 | 51,703 | 56,501 | |||||||||||||||

| Provision for income tax | 2,926 | 3,425 | 1,915 | 2,847 | 2,784 | |||||||||||||||

| Net income | 13,456 | 11,596 | 6,800 | 9,012 | 10,270 | |||||||||||||||

| As of and for the Three Month Period | ||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | March 31, 2024 | December 31, 2023 | September 30, 2023 | ||||||||||||||||

| Balance Sheet Data: | ||||||||||||||||||||

| Cash and cash equivalents | $ | 484,026 | $ | 487,245 | $ | 515,128 | $ | 483,128 | $ | 474,946 | ||||||||||

| Investment securities | 48,620 | 49,213 | 50,090 | 150,364 | 141,489 | |||||||||||||||

| Loans held for sale | 7,565 | — | 797 | — | — | |||||||||||||||

| Loans receivable | 3,418,832 | 3,326,460 | 3,199,554 | 3,026,092 | 2,967,035 | |||||||||||||||

| Allowance for credit losses | (170,263 | ) | (147,914 | ) | (139,258 | ) | (116,958 | ) | (101,085 | ) | ||||||||||

| Total assets | 4,065,821 | 3,961,546 | 3,865,258 | 3,753,366 | 3,678,265 | |||||||||||||||

| Interest bearing deposits | 3,047,861 | 2,949,643 | 2,888,867 | 2,735,161 | 2,637,914 | |||||||||||||||

| Noninterest bearing deposits | 579,427 | 593,789 | 574,112 | 625,202 | 651,786 | |||||||||||||||

| Core deposits (1) | 3,190,869 | 3,528,339 | 3,447,864 | 3,342,004 | 3,269,082 | |||||||||||||||

| Total deposits | 3,627,288 | 3,543,432 | 3,462,979 | 3,360,363 | 3,289,700 | |||||||||||||||

| Total borrowings | 47,847 | 47,810 | 47,771 | 47,734 | 47,695 | |||||||||||||||

| Total shareholders’ equity | 331,930 | 316,693 | 303,709 | 294,978 | 284,450 | |||||||||||||||

| Share and Per Share Data (2): | ||||||||||||||||||||

| Earnings per share – basic | $ | 1.00 | $ | 0.86 | $ | 0.51 | $ | 0.68 | $ | 0.77 | ||||||||||

| Earnings per share – diluted | $ | 0.97 | $ | 0.84 | $ | 0.50 | $ | 0.66 | $ | 0.75 | ||||||||||

| Dividends per share | — | — | — | — | — | |||||||||||||||

| Book value per share (3) | $ | 24.51 | $ | 23.54 | $ | 22.65 | $ | 22.17 | $ | 21.38 | ||||||||||

| Tangible book value per share (4) | $ | 24.51 | $ | 23.54 | $ | 22.65 | $ | 22.17 | $ | 21.38 | ||||||||||

| Weighted avg outstanding shares – basic | 13,447,066 | 13,412,667 | 13,340,997 | 13,286,828 | 13,285,974 | |||||||||||||||

| Weighted avg outstanding shares – diluted | 13,822,270 | 13,736,508 | 13,676,917 | 13,676,513 | 13,675,833 | |||||||||||||||

| Shares outstanding at end of period | 13,543,282 | 13,453,805 | 13,407,320 | 13,304,339 | 13,302,449 | |||||||||||||||

| Stock options outstanding at end of period | 198,370 | 286,119 | 309,069 | 354,969 | 356,359 | |||||||||||||||

| See footnotes that follow the tables below | ||||||||||||||||||||

| As of and for the Three Month Period | ||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | March 31, 2024 | December 31, 2023 | September 30, 2023 | ||||||||||||||||

| Credit Quality Data: | ||||||||||||||||||||

| Nonperforming assets (5) to total assets | 1.34 | % | 1.34 | % | 1.42 | % | 1.43 | % | 1.18 | % | ||||||||||

| Nonperforming assets (5) to loans receivable and OREO | 1.60 | % | 1.60 | % | 1.71 | % | 1.78 | % | 1.47 | % | ||||||||||

| Nonperforming loans (5) to total loans receivable | 1.60 | % | 1.60 | % | 1.71 | % | 1.78 | % | 1.47 | % | ||||||||||

| Allowance for credit losses to nonperforming loans | 311.5 | % | 278.1 | % | 253.8 | % | 217.2 | % | 232.2 | % | ||||||||||

| Allowance for credit losses to total loans receivable | 4.98 | % | 4.45 | % | 4.35 | % | 3.86 | % | 3.41 | % | ||||||||||

| Gross charge-offs | $ | 53,305 | $ | 55,207 | $ | 58,994 | $ | 47,652 | $ | 37,879 | ||||||||||

| Gross recoveries | $ | 4,069 | $ | 1,973 | $ | 1,776 | $ | 2,781 | $ | 1,045 | ||||||||||

| Net charge-offs to average loans (6) | 5.65 | % | 6.57 | % | 7.34 | % | 5.92 | % | 4.77 | % | ||||||||||

| Capital Ratios: | ||||||||||||||||||||

| Company | ||||||||||||||||||||

| Tier 1 leverage capital | 8.40 | % | 8.31 | % | 8.24 | % | 8.10 | % | 8.03 | % | ||||||||||

| Common equity Tier 1 risk-based capital | 9.26 | % | 9.03 | % | 8.98 | % | 9.10 | % | 9.00 | % | ||||||||||

| Tier 1 risk-based capital | 9.35 | % | 9.13 | % | 9.08 | % | 9.20 | % | 9.11 | % | ||||||||||

| Total risk-based capital | 11.90 | % | 11.70 | % | 11.70 | % | 11.87 | % | 11.80 | % | ||||||||||

| Bank | ||||||||||||||||||||

| Tier 1 leverage capital | 9.29 | % | 9.24 | % | 9.19 | % | 9.06 | % | 8.99 | % | ||||||||||

| Common equity Tier 1 risk-based capital | 10.36 | % | 10.15 | % | 10.14 | % | 10.30 | % | 10.21 | % | ||||||||||

| Tier 1 risk-based capital | 10.36 | % | 10.15 | % | 10.14 | % | 10.30 | % | 10.21 | % | ||||||||||

| Total risk-based capital | 11.65 | % | 11.44 | % | 11.43 | % | 11.58 | % | 11.48 | % | ||||||||||

(1) Core deposits are defined as all deposits excluding brokered and all time deposits.

(2) Share and per share amounts are based on total actual or average common shares outstanding, as applicable.

(3) We calculate book value per share as total shareholders’ equity at the end of the relevant period divided by the outstanding number of our common shares at the end of each period.

(4) Tangible book value per share is a non-GAAP financial measure. We calculate tangible book value per share as total shareholders’ equity at the end of the relevant period, less goodwill and other intangible assets, divided by the outstanding number of our common shares at the end of each period. The most directly comparable GAAP financial measure is book value per share. We had no goodwill or other intangible assets as of any of the dates indicated. As a result, tangible book value per share is the same as book value per share as of each of the dates indicated.

(5) Nonperforming assets and nonperforming loans include loans 90+ days past due and accruing interest.

(6) Annualized calculations.

Key Performance Ratios

Return on average assets ("ROA") was 1.34% for the quarter ended September 30, 2024 compared to 1.21% and 1.13% for the quarters ended June 30, 2024 and September 30, 2023, respectively. ROA for the quarter ended September 30, 2024, increased 0.13% and 0.21% compared to June 30, 2024 and September 30, 2023, respectively. Noninterest expenses were higher for the quarter ended September 30, 2024 compared to the quarters ended June 30, 2024 and September 30, 2023 largely due to an increase in BaaS loan expense, which is directly related to the increase in the amount of interest earned on CCBX loans.

The following table shows the Company’s key performance ratios for the periods indicated.

| Three Months Ended | |||||||||||||||

| (unaudited) | September 30, 2024 | June 30, 2024 | March 31, 2024 | December 31, 2023 | September 30, 2023 | ||||||||||

| Return on average assets (1) | 1.34 | % | 1.21 | % | 0.73 | % | 0.97 | % | 1.13 | % | |||||

| Return on average equity (1) | 16.67 | % | 15.22 | % | 9.21 | % | 12.35 | % | 14.60 | % | |||||

| Yield on earnings assets (1) | 10.79 | % | 10.49 | % | 10.07 | % | 9.77 | % | 10.08 | % | |||||

| Yield on loans receivable (1) | 11.43 | % | 11.23 | % | 10.85 | % | 10.71 | % | 10.84 | % | |||||

| Cost of funds (1) | 3.62 | % | 3.60 | % | 3.52 | % | 3.39 | % | 3.18 | % | |||||

| Cost of deposits (1) | 3.59 | % | 3.58 | % | 3.49 | % | 3.36 | % | 3.14 | % | |||||

| Net interest margin (1) | 7.41 | % | 7.13 | % | 6.78 | % | 6.61 | % | 7.10 | % | |||||

| Noninterest expense to average assets (1) | 6.54 | % | 6.14 | % | 6.04 | % | 5.56 | % | 6.23 | % | |||||

| Noninterest income to average assets (1) | 7.98 | % | 7.30 | % | 9.38 | % | 6.95 | % | 3.81 | % | |||||

| Efficiency ratio | 43.10 | % | 43.19 | % | 37.88 | % | 41.58 | % | 58.36 | % | |||||

| Loans receivable to deposits (2) | 94.46 | % | 93.88 | % | 92.42 | % | 90.05 | % | 90.19 | % | |||||

(1) Annualized calculations shown for quarterly periods presented.

(2) Includes loans held for sale.

Management Outlook; CEO Eric Sprink

“As we look ahead to the fourth quarter and 2025, we remain laser focused on building out our technology and risk management infrastructure to more efficiently support our next phase of growth within CCBX. While the balance sheet re-mix earlier this year resulted in a short-term reduction to income, we continue to make strategic decisions which are enhancing credit quality, generating passive fee income, strengthening our talent and growing relationships with established and prospective CCBX partners all of which are expected to position Coastal to be more profitable in 2025.”

Coastal Financial Corporation Overview

The Company has one main subsidiary, the Bank which consists of three segments: CCBX, the community bank and treasury & administration. The CCBX segment includes all of our BaaS activities, the community bank segment includes all community banking activities, and the treasury & administration segment includes treasury management, overall administration and all other aspects of the Company.

CCBX Performance Update

Our CCBX segment continues to evolve, and we have 22 relationships, at varying stages, as of September 30, 2024. We continue to refine the criteria for CCBX partnerships, are exiting relationships where it makes sense for us to do so and are focusing on larger more established partners, with experienced management teams, existing customer bases and strong financial positions.

We are expanding product offerings with our existing CCBX partners. We believe that launching new products with existing partners positions us to reach a wide and established customer base with a modest increase in regulatory risk given we have already vetted these partners and have operational history. Products launched earlier in the year with existing partners have gained traction and are growing the balance sheet and increasing income. We continue to sell loans as part of our strategy to balance partner and lending limits, and manage the loan portfolio and credit quality. We retain a portion of the fee income for our role in processing transactions on sold credit card balances. This is expected to provide an on-going and passive revenue stream with no on balance sheet risk.

The following table illustrates the activity and evolution in CCBX relationships for the periods presented.

| As of | ||||

| (unaudited) | September 30, 2024 | June 30, 2024 | September 30, 2023 | |

| Active | 19 | 19 | 18 | |

| Friends and family / testing | 1 | 1 | 1 | |

| Implementation / onboarding | 1 | 1 | 1 | |

| Signed letters of intent | 1 | 0 | 1 | |

| Wind down - active but preparing to exit relationship | 0 | 0 | 1 | |

| Total CCBX relationships | 22 | 21 | 22 | |

CCBX loans increased $106.9 million, or 7.6%, despite selling $423.7 million loans during the three months ended September 30, 2024 to $1.52 billion, while we continued to enhance credit standards on new CCBX loan originations. In accordance with the program agreement for one partner, effective April 1, 2024, the portion of the CCBX portfolio that we are responsible for losses on decreased from 10% to 5%. At September 30, 2024 the portion of this portfolio for which we are responsible represented $19.8 million in loans.

The following table details the CCBX loan portfolio:

| CCBX | As of | ||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | September 30, 2023 | |||||||||||||||||||

| (dollars in thousands; unaudited) | Balance | % to Total | Balance | % to Total | Balance | % to Total | |||||||||||||||

| Commercial and industrial loans: | |||||||||||||||||||||

| Capital call lines | $ | 103,924 | 6.8 | % | $ | 109,133 | 7.7 | % | $ | 114,174 | 9.6 | % | |||||||||

| All other commercial & industrial loans | 36,494 | 2.4 | 41,731 | 3.0 | 58,869 | 5.0 | |||||||||||||||

| Real estate loans: | |||||||||||||||||||||

| Residential real estate loans | 265,402 | 17.5 | 287,950 | 20.4 | 251,775 | 21.3 | |||||||||||||||

| Consumer and other loans: | |||||||||||||||||||||

| Credit cards | 633,691 | 41.6 | 549,241 | 38.7 | 440,993 | 37.3 | |||||||||||||||

| Other consumer and other loans | 482,228 | 31.7 | 426,809 | 30.2 | 316,987 | 26.8 | |||||||||||||||

| Gross CCBX loans receivable | 1,521,739 | 100.0 | % | 1,414,864 | 100.0 | % | 1,182,798 | 100.0 | % | ||||||||||||

| Net deferred origination (fees) costs | (447 | ) | (438 | ) | (424 | ) | |||||||||||||||

| Loans receivable | $ | 1,521,292 | $ | 1,414,426 | $ | 1,182,374 | |||||||||||||||

| Loan Yield - CCBX (1)(2) | 17.35 | % | 17.77 | % | 17.05 | % | |||||||||||||||

(1) CCBX yield does not include the impact of BaaS loan expense. BaaS loan expense represents the amount paid or payable to partners for credit enhancements and originating & servicing CCBX loans. See reconciliation of the non-GAAP measures at the end of this earnings release for the impact of BaaS loan expense on CCBX loan yield.

(2) Loan yield is annualized for the three months ended for each period presented and includes loans held for sale and nonaccrual loans.

The increase in CCBX loans in the quarter ended September 30, 2024, includes an increase of $139.9 million or 14.3%, in consumer and other loans, partially offset by a $22.5 million, or 7.8%, decrease in residential real estate loans and a decrease of $5.2 million, or 4.8%, in capital call lines as a result of normal balance fluctuations and business activities. We continue to monitor and manage the CCBX loan portfolio, and sold $423.7 million in CCBX loans during the quarter ended September 30, 2024 compared to sales of $155.2 million in the quarter ended June 30, 2024. We continue to reposition ourselves by managing CCBX credit and concentration levels in an effort to optimize our loan portfolio and generate off balance sheet fee income.

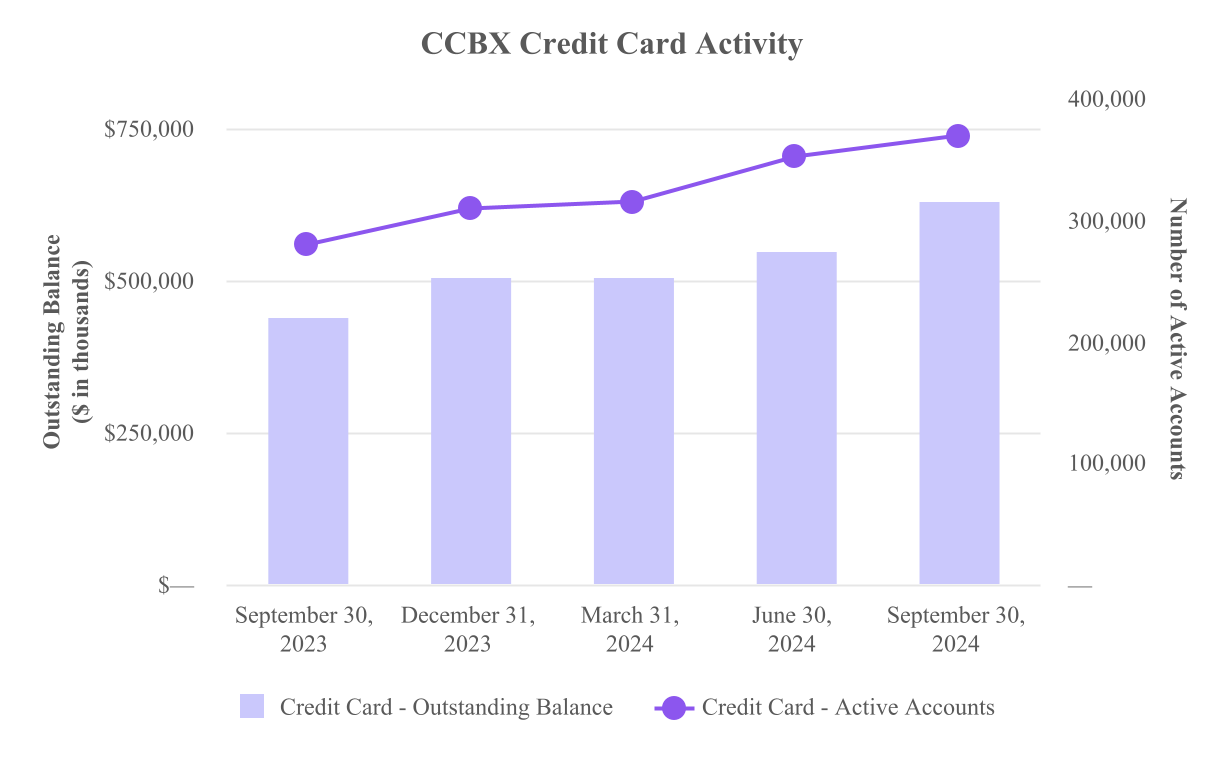

Our credit card program through CCBX continues to grow in dollars and number of active cards as shown in the graph below:

The following table details the CCBX deposit portfolio:

| CCBX | As of | ||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | September 30, 2023 | |||||||||||||||||||

| (dollars in thousands; unaudited) | Balance | % to Total | Balance | % to Total | Balance | % to Total | |||||||||||||||

| Demand, noninterest bearing | $ | 60,655 | 2.9 | % | $ | 62,234 | 3.0 | % | $ | 67,782 | 3.9 | % | |||||||||

| Interest bearing demand and money market | 1,991,858 | 94.6 | 1,989,105 | 96.7 | 1,679,921 | 95.9 | |||||||||||||||

| Savings | 5,204 | 0.3 | 5,150 | 0.3 | 4,529 | 0.2 | |||||||||||||||

| Total core deposits | 2,057,717 | 97.8 | 2,056,489 | 100.0 | 1,752,232 | 100.0 | |||||||||||||||

| Other deposits | 47,046 | 2.2 | — | 0.0 | — | — | |||||||||||||||

| Total CCBX deposits | $ | 2,104,763 | 100.0 | % | $ | 2,056,489 | 100.0 | % | $ | 1,752,232 | 100.0 | % | |||||||||

| Cost of deposits (1) | 4.82 | % | 4.92 | % | 4.80 | % | |||||||||||||||

(1) Cost of deposits is annualized for the three months ended for each period presented.

CCBX deposits increased $48.3 million, or 2.3%, in the three months ended September 30, 2024 to $2.10 billion. This excludes the $214.5 million in CCBX deposits that were transferred off balance sheet for increased Federal Deposit Insurance Corporation ("FDIC") insurance coverage purposes, compared to $117.7 million for the quarter ended June 30, 2024. Amounts in excess of FDIC insurance coverage are transferred, using a third party facilitator/vendor sweep product, to participating financial institutions.

Community Bank Performance Update

In the quarter ended September 30, 2024, the community bank saw net loans decrease $14.5 million, or 0.8%, to $1.90 billion.

The following table details the Community Bank loan portfolio:

| Community Bank | As of | ||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | September 30, 2023 | |||||||||||||||||||

| (dollars in thousands; unaudited) | Balance | % to Total | Balance | % to Total | Balance | % to Total | |||||||||||||||

| Commercial and industrial loans | $ | 152,161 | 8.0 | % | $ | 144,436 | 7.5 | % | $ | 158,232 | 8.8 | % | |||||||||

| Real estate loans: | |||||||||||||||||||||

| Construction, land and land development loans | 163,051 | 8.6 | 173,064 | 9.0 | 167,686 | 9.4 | |||||||||||||||

| Residential real estate loans | 212,467 | 11.2 | 229,639 | 12.0 | 225,372 | 12.6 | |||||||||||||||

| Commercial real estate loans | 1,362,452 | 71.5 | 1,357,979 | 70.8 | 1,237,849 | 69.1 | |||||||||||||||

| Consumer and other loans: | |||||||||||||||||||||

| Other consumer and other loans | 14,173 | 0.7 | 14,220 | 0.7 | 2,483 | 0.1 | |||||||||||||||

| Gross Community Bank loans receivable | 1,904,304 | 100.0 | % | 1,919,338 | 100.0 | % | 1,791,622 | 100.0 | % | ||||||||||||

| Net deferred origination fees | (6,764 | ) | (7,304 | ) | (6,961 | ) | |||||||||||||||

| Loans receivable | $ | 1,897,540 | $ | 1,912,034 | $ | 1,784,661 | |||||||||||||||

| Loan Yield(1) | 6.64 | % | 6.52 | % | 6.20 | % | |||||||||||||||

(1) Loan yield is annualized for the three months ended for each period presented and includes loans held for sale and nonaccrual loans.

Community bank loans had a $10.0 million decrease in construction, land and land development loans, partially offset by an increase of $7.7 million in commercial and industrial loans and an increase in commercial real estate loans of $4.5 million during the quarter ended September 30, 2024; consumer and other loans were flat.

The following table details the community bank deposit portfolio:

| Community Bank | As of | ||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | September 30, 2023 | |||||||||||||||||||

| (dollars in thousands; unaudited) | Balance | % to Total | Balance | % to Total | Balance | % to Total | |||||||||||||||

| Demand, noninterest bearing | $ | 518,772 | 34.1 | % | $ | 531,555 | 35.6 | % | $ | 584,004 | 37.9 | % | |||||||||

| Interest bearing demand and money market | 552,108 | 36.3 | 876,668 | 59.0 | 852,747 | 55.5 | |||||||||||||||

| Savings | 62,272 | 4.1 | 63,627 | 4.3 | 80,099 | 5.2 | |||||||||||||||

| Total core deposits | 1,133,152 | 74.5 | 1,471,850 | 98.9 | 1,516,850 | 98.6 | |||||||||||||||

| Other deposits | 373,681 | 24.5 | 1 | 0.0 | 1 | 0.0 | |||||||||||||||

| Time deposits less than $100,000 | 6,305 | 0.4 | 6,741 | 0.5 | 8,635 | 0.6 | |||||||||||||||

| Time deposits $100,000 and over | 9,387 | 0.6 | 8,351 | 0.6 | 11,982 | 0.8 | |||||||||||||||

| Total Community Bank deposits | $ | 1,522,525 | 100.0 | % | $ | 1,486,943 | 100.0 | % | $ | 1,537,468 | 100.0 | % | |||||||||

| Cost of deposits(1) | 1.92 | % | 1.77 | % | 1.31 | % | |||||||||||||||

(1) Cost of deposits is annualized for the three months ended for each period presented.

Community bank deposits increased $35.6 million, or 2.4%, during the three months ended September 30, 2024 to $1.52 billion. This is the second consecutive quarter of growth after allowing higher rate balances to run-off earlier in the year. The community bank segment includes noninterest bearing deposits of $518.8 million, or 34.1%, of total community bank deposits, resulting in a cost of deposits of 1.92%, which compared to 1.77% for the quarter ended June 30, 2024.

Net Interest Income and Margin Discussion

Net interest income was $72.2 million for the quarter ended September 30, 2024, an increase of $5.9 million, or 9.0%, from $66.2 million for the quarter ended June 30, 2024, and an increase of $10.0 million, or 16.0%, from $62.2 million for the quarter ended September 30, 2023. The increase in net interest income compared to June 30, 2024, was a result of increased interest income due to an increase in average loans receivable partially offset by an increase in cost of funds. The increase in net interest income compared to September 30, 2023 was largely related to increased yield on loans resulting from higher interest rates and growth in higher yielding loans partially offset by an increase in cost of funds relating to higher interest rates and growth in interest bearing deposits.

Net interest margin was 7.41% for the three months ended September 30, 2024, compared to 7.13% for the three months ended June 30, 2024, with the increase primarily due to higher loan yields. Net interest margin was 7.10% for the three months ended September 30, 2023. The increase in net interest margin for the three months ended September 30, 2024 compared to the three months ended September 30, 2023 was largely due to an increase in loan yield partially offset by higher interest rates on interest bearing deposits. Interest and fees on loans receivable increased $8.6 million, or 9.5%, to $99.6 million for the three months ended September 30, 2024, compared to $90.9 million for the three months ended June 30, 2024, and increased $15.9 million, or 19.1%, compared to $83.7 million for the three months ended September 30, 2023, due to an increase in outstanding balances and higher interest rates.

Average investment securities decreased $795,000 to $49.0 million compared to the three months ended June 30, 2024 and decreased $69.0 million compared to the three months ended September 30, 2023 as a result of maturing securities.

Cost of funds was 3.62% for the quarter ended September 30, 2024, an increase of 2 basis points from the quarter ended June 30, 2024 and an increase of 44 basis points from the quarter ended September 30, 2023. Cost of deposits for the quarter ended September 30, 2024 was 3.59%, compared to 3.58% for the quarter ended June 30, 2024, and 3.14% for the quarter ended September 30, 2023. The increased cost of funds and deposits compared to June 30, 2024 and September 30, 2023 was due to the continued high interest rate environment. The late September reduction in the Fed funds rate is expected to help to lower our cost of deposits in future periods.

The following table summarizes the average yield on loans receivable and cost of deposits:

| For the Three Months Ended | ||||||||||||||||||

| September 30, 2024 | June 30, 2024 | September 30, 2023 | ||||||||||||||||

| Yield on Loans (2) | Cost of Deposits (2) | Yield on Loans (2) | Cost of Deposits (2) | Yield on Loans (2) | Cost of Deposits (2) | |||||||||||||

| Community Bank | 6.64 | % | 1.92 | % | 6.52 | % | 1.77 | % | 6.20 | % | 1.31 | % | ||||||

| CCBX (1) | 17.35 | % | 4.82 | % | 17.77 | % | 4.92 | % | 17.05 | % | 4.80 | % | ||||||

| Consolidated | 11.43 | % | 3.59 | % | 11.23 | % | 3.58 | % | 10.84 | % | 3.14 | % | ||||||

(1) CCBX yield on loans does not include the impact of BaaS loan expense. BaaS loan expense represents the amount paid or payable to partners for credit and fraud enhancements and originating & servicing CCBX loans. To determine Net BaaS loan income earned from CCBX loan relationships, the Company takes BaaS loan interest income and deducts BaaS loan expense to arrive at Net BaaS loan income which can be compared to interest income on the Company’s community bank loans. See reconciliation of the non-GAAP measures at the end of this earnings release for the impact of BaaS loan expense on CCBX loan yield.

(2) Annualized calculations for periods shown.

The following tables illustrates how BaaS loan interest income is affected by BaaS loan expense resulting in net BaaS loan income and the associated yield:

| For the Three Months Ended | ||||||||||||||||||

| September 30, 2024 | June 30, 2024 | September 30, 2023 | ||||||||||||||||

| (dollars in thousands, unaudited) | Income / Expense | Income / expense divided by average CCBX loans (2) | Income / Expense | Income / expense divided by average CCBX loans(2) | Income / Expense | Income / expense divided by average CCBX loans (2) | ||||||||||||

| BaaS loan interest income | $ | 67,692 | 17.35 | % | $ | 60,203 | 17.77 | % | $ | 56,279 | 17.05 | % | ||||||

| Less: BaaS loan expense | 32,612 | 8.36 | % | 29,076 | 8.58 | % | 23,003 | 6.97 | % | |||||||||

| Net BaaS loan income (1) | $ | 35,080 | 8.99 | % | $ | 31,127 | 9.19 | % | $ | 33,276 | 10.08 | % | ||||||

| Average BaaS Loans(3) | $ | 1,552,443 | $ | 1,362,343 | $ | 1,309,380 | ||||||||||||

(1) A reconciliation of the non-GAAP measures are set forth at the end of this earnings release.

(2) Annualized calculations shown for quarterly periods presented.

(3) Includes loans held for sale.

Noninterest Income Discussion

Noninterest income was $80.1 million for the three months ended September 30, 2024, an increase of $10.2 million from $69.9 million for the three months ended June 30, 2024, and an increase of $45.5 million from $34.6 million for the three months ended September 30, 2023. The increase in noninterest income over the quarter ended June 30, 2024 was primarily due to an increase of $9.9 million in total BaaS income. The $9.9 million increase in total BaaS income included a $9.3 million increase in BaaS credit enhancements related to the provision for credit losses, a $300,000 increase in BaaS fraud enhancements, and an increase of $340,000 in BaaS program income. The increase in BaaS program income is largely due to higher servicing and other BaaS fees, transaction fees and interchange fees and our primary BaaS source for recurring fee income (see “Appendix B” for more information on the accounting for BaaS allowance for credit losses and credit and fraud enhancements). Additionally, other income increased $229,000 largely due to increased incoming ACH activity.

The $45.5 million increase in noninterest income over the quarter ended September 30, 2023 was primarily due to a $43.4 million increase in BaaS credit and fraud enhancements, and an increase of $2.0 million in BaaS program income.

Noninterest Expense Discussion

Total noninterest expense increased $6.8 million to $65.6 million for the three months ended September 30, 2024, compared to $58.8 million for the three months ended June 30, 2024, and increased $9.1 million from $56.5 million for the three months ended September 30, 2023. The increase in noninterest expense for the quarter ended September 30, 2024, as compared to the quarter ended June 30, 2024, was primarily due to a $3.8 million increase in BaaS expense (including a $300,000 increase in BaaS fraud expense and a $3.5 million increase in BaaS loan expense). BaaS loan expense represents the amount paid or payable to partners for credit enhancements, fraud enhancements, and originating & servicing CCBX loans. BaaS fraud expense represents non-credit fraud losses on partner’s customer loan and deposit accounts. A portion of this expense is realized during the quarter in which the loss occurs, and a portion is estimated based on historical or other information from our partners, partially offset by a $1.5 million increase in excise taxes (due to the recording of $1.2 million business and occupation tax credit from the State of Washington which resulted in the recognition of a net credit of $706,000 for the quarter ended June 30, 2024, compared to expense of $762,000 for the quarter ended September 30, 2024). We also recorded an increase of $587,000 in data processing and software licenses as a result of our continued investment in our infrastructure and the automation of our processes so that they are scalable and an increase of $499,000 in point of sale expenses as a result of increased partner transaction activity.

The increase in noninterest expenses for the quarter ended September 30, 2024 compared to the quarter ended September 30, 2023 was largely due to an increase of $8.8 million in BaaS partner expense (including a $9.6 million increase in BaaS loan expense partially offset by a decrease of $766,000 in BaaS fraud expense), a $1.1 million increase in data processing and software licenses due to enhancements in technology, and a $526,000 increase in occupancy expense, largely due to higher software depreciation/amortization expense, partially offset by a $986,000 decrease in salary and employee benefits largely as a result of some one-time costs that were expensed in the quarter ended September 30, 2023 for which there was no similar expense in the current quarter, and an $850,000 decrease in legal and professional expenses as a result of risk management and projects being completed.

Provision for Income Taxes

The provision for income taxes was $2.9 million for the three months ended September 30, 2024, $3.4 million for the three months ended June 30, 2024 and $2.8 million for the third quarter of 2023. The income tax provision was lower for the three months ended September 30, 2024 compared to the quarter ended June 30, 2024 as a result of the deductibility of certain equity awards which reduced tax expense despite net income being higher and higher than the quarter ended September 30, 2023, primarily due to higher net income compared to that quarter.

The Company is subject to various state taxes that are assessed as CCBX activities and employees expand into other states, which has increased the overall tax rate used in calculating the provision for income taxes in the current and future periods. The Company uses a federal statutory tax rate of 21.0% as a basis for calculating provision for federal income taxes and 2.62% for calculating the provision for state income taxes.

Financial Condition Overview

Total assets increased $104.3 million, or 2.6%, to $4.07 billion at September 30, 2024 compared to $3.96 billion at June 30, 2024. The increase is primarily due to stronger loan growth partially offset by lower cash balances. Total loans receivable increased $92.4 million to $3.42 billion at September 30, 2024, from $3.33 billion at June 30, 2024.

As of September 30, 2024, the Company had the capacity to borrow up to a total of $656.3 million from the Federal Reserve Bank discount window and Federal Home Loan Bank, and an additional $50.0 million from a correspondent bank no borrowings outstanding on these lines as of September 30, 2024.

The Company had a cash balance of $5.9 million as of September 30, 2024, which is retained for general operating purposes, including debt repayment, and for funding $530,000 in commitments to bank technology funds.

Uninsured deposits were $542.2 million as of September 30, 2024, compared to $532.9 million as of June 30, 2024.

Total shareholders’ equity increased $15.2 million since June 30, 2024. The increase in shareholders’ equity was primarily due to $13.5 million in net earnings, combined with an increase of $1.8 million in common stock outstanding as a result of equity awards exercised during the three months ended September 30, 2024.

The Company and the Bank remained well capitalized at September 30, 2024, as summarized in the following table.

| (unaudited) | Coastal Community Bank | Coastal Financial Corporation | Minimum Well Capitalized Ratios under Prompt Corrective Action (1) | ||||||

| Tier 1 Leverage Capital (to average assets) | 9.29 | % | 8.40 | % | 5.00 | % | |||

| Common Equity Tier 1 Capital (to risk-weighted assets) | 10.36 | % | 9.26 | % | 6.50 | % | |||

| Tier 1 Capital (to risk-weighted assets) | 10.36 | % | 9.35 | % | 8.00 | % | |||

| Total Capital (to risk-weighted assets) | 11.65 | % | 11.90 | % | 10.00 | % | |||

(1) Presents the minimum capital ratios for an insured depository institution, such as the Bank, to be considered well capitalized under the Prompt Corrective Action framework. The minimum requirements for the Company to be considered well capitalized under Regulation Y include to maintain, on a consolidated basis, a total risk-based capital ratio of 10.0 percent or greater and a tier 1 risk-based capital ratio of 6.0 percent or greater.

Asset Quality

The total allowance for credit losses was $170.3 million and 4.98% of loans receivable at September 30, 2024 compared to $147.9 million and 4.45% at June 30, 2024 and $101.1 million and 3.41% at September 30, 2023. The allowance for credit loss allocated to the CCBX portfolio was $150.1 million and 9.87% of CCBX loans receivable at September 30, 2024, with $20.1 million of allowance for credit loss allocated to the community bank or 1.06% of total community bank loans receivable.

The following table details the allocation of the allowance for credit loss as of the period indicated:

| As of September 30, 2024 | As of June 30, 2024 | As of September 30, 2023 | ||||||||||||||||||||||||||||||||||

| (dollars in thousands; unaudited) | Community Bank | CCBX | Total | Community Bank | CCBX | Total | Community Bank | CCBX | Total | |||||||||||||||||||||||||||

| Loans receivable | $ | 1,897,540 | $ | 1,521,292 | $ | 3,418,832 | $ | 1,912,034 | $ | 1,414,426 | $ | 3,326,460 | $ | 1,784,661 | $ | 1,182,374 | $ | 2,967,035 | ||||||||||||||||||

| Allowance for credit losses | (20,132 | ) | (150,131 | ) | (170,263 | ) | (21,045 | ) | (126,869 | ) | (147,914 | ) | (21,316 | ) | (79,769 | ) | (101,085 | ) | ||||||||||||||||||

| Allowance for credit losses to total loans receivable | 1.06 | % | 9.87 | % | 4.98 | % | 1.10 | % | 8.97 | % | 4.45 | % | 1.19 | % | 6.75 | % | 3.41 | % | ||||||||||||||||||

Net charge-offs totaled $49.2 million for the quarter ended September 30, 2024, compared to $53.2 million for the quarter ended June 30, 2024 and $36.8 million for the quarter ended September 30, 2023. Net charge-offs as a percent of average loans decreased to 5.65% for the quarter ended September 30, 2024 compared to 6.57% for the quarter ended June 30, 2024, which we believe is a result of the steps we took manage our credit quality. CCBX partner agreements provide for a credit enhancement that covers the net-charge-offs on CCBX loans and negative deposit accounts by indemnifying or reimbursing incurred losses, except in accordance with the program agreement for one partner where the Company was responsible for credit losses on approximately 5% of a $400.8 million loan portfolio. At September 30, 2024, our portion of this portfolio represented $19.8 million in loans. Net charge-offs for this $19.8 million in loans were $1.1 million for the three months ended September 30, 2024, compared to $1.3 million for the three months ended June 30, 2024 and $579,000 for the three months ended September 30, 2023.

The following table details net charge-offs for the community bank and CCBX for the period indicated:

| Three Months Ended | ||||||||||||||||||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | September 30, 2023 | ||||||||||||||||||||||||||||||||||

| (dollars in thousands; unaudited) | Community Bank | CCBX | Total | Community Bank | CCBX | Total | Community Bank | CCBX | Total | |||||||||||||||||||||||||||

| Gross charge-offs | $ | 398 | $ | 52,907 | $ | 53,305 | $ | 2 | $ | 55,205 | $ | 55,207 | $ | 3 | $ | 37,876 | $ | 37,879 | ||||||||||||||||||

| Gross recoveries | (3 | ) | (4,066 | ) | (4,069 | ) | (4 | ) | (1,969 | ) | (1,973 | ) | (3 | ) | (1,042 | ) | (1,045 | ) | ||||||||||||||||||

| Net charge-offs | $ | 395 | $ | 48,841 | $ | 49,236 | $ | (2 | ) | $ | 53,236 | $ | 53,234 | $ | — | $ | 36,834 | $ | 36,834 | |||||||||||||||||

| Net charge-offs to average loans (1) | 0.08 | % | 12.52 | % | 5.65 | % | 0.00 | % | 15.72 | % | 6.57 | % | 0.00 | % | 11.16 | % | 4.77 | % | ||||||||||||||||||

(1) Annualized calculations shown for periods presented.

During the quarter ended September 30, 2024, a $72.1 million provision for credit losses - loans was recorded for CCBX partner loans based on management’s analysis, compared to the $62.2 million provision for credit losses - loans that was recorded for CCBX for the quarter ended June 30, 2024. CCBX loans have a higher level of expected losses than our community bank loans, which is reflected in the factors for the allowance for credit losses. Agreements with our CCBX partners provide for a credit enhancement which protects the Bank by indemnifying or reimbursing incurred losses.

In accordance with accounting guidance, we estimate and record a provision for expected losses for these CCBX loans and reclassified negative deposit accounts. When the provision for CCBX credit losses and provision for unfunded commitments is recorded, a credit enhancement asset is also recorded on the balance sheet through noninterest income (BaaS credit enhancements). Expected losses are recorded in the allowance for credit losses. The credit enhancement asset is relieved when credit enhancement recoveries are received from the CCBX partner. If our partner is unable to fulfill their contracted obligations then the Bank could be exposed to additional credit losses. Management regularly evaluates and manages this counterparty risk.

The factors used in management’s analysis for community bank credit losses indicated that a provision recapture of $519,000 and was needed for the quarter ended September 30, 2024 compared to a provision recapture of $341,000 and provision of $664,000 for the quarters ended June 30, 2024 and September 30, 2023, respectively. The recapture in the current period was largely due to a change in remaining average lives of community bank loans.

The following table details the provision expense/(recapture) for the community bank and CCBX for the period indicated:

| Three Months Ended | |||||||||||

| (dollars in thousands; unaudited) | September 30, 2024 | June 30, 2024 | September 30, 2023 | ||||||||

| Community bank | $ | (519 | ) | $ | (341 | ) | $ | 664 | |||

| CCBX | 72,104 | 62,231 | 26,493 | ||||||||

| Total provision expense | $ | 71,585 | $ | 61,890 | $ | 27,157 | |||||

At September 30, 2024, our nonperforming assets were $54.7 million, or 1.34%, of total assets, compared to $53.2 million, or 1.34%, of total assets, at June 30, 2024, and $43.5 million, or 1.18%, of total assets, at September 30, 2023. These ratios are impacted by nonperforming CCBX loans that are covered by CCBX partner credit enhancements. As of September 30, 2024, $52.0 million of the $53.6 million in nonperforming CCBX loans were covered by CCBX partner credit enhancements described above.

Nonperforming assets increased $1.5 million during the quarter ended September 30, 2024, compared to the quarter ended June 30, 2024. This change is largely due to an increase in CCBX nonaccrual loans partially offset by a decrease in community bank nonaccrual loans. CCBX nonaccrual loans increased $8.0 million as a result of a new collection practice that places certain loans on nonaccrual status to improve collectability, $5.3 million of these loans are less than 90 days past due as of September 30, 2024. CCBX loans that are past due 90 days or more and still accruing was $45.6 million for the quarter ended September 30, 2024 compared to $45.2 million for the quarter ended June 30, 2024. As a result of the type of loans (primarily consumer loans) originated through our CCBX partners we anticipate that balances 90 days past due or more and still accruing will generally increase as those loan portfolios grow. Installment/closed-end and revolving/open-end consumer loans originated through CCBX lending partners will continue to accrue interest until 120 and 180 days past due, respectively and are reported as substandard, 90 days or more days past due and still accruing. There were no repossessed assets or other real estate owned at September 30, 2024. Our nonperforming loans to loans receivable ratio was 1.60% at September 30, 2024, compared to 1.60% at June 30, 2024, and 1.47% at September 30, 2023.

For the quarter ended September 30, 2024, there were $395,000 community bank net charge-offs and $1.1 million nonperforming community bank loans. For the quarter ended September 30, 2024 $48.8 million in net charge-offs were recorded on CCBX loans. These CCBX loans have a higher level of expected losses than our community bank loans, which is reflected in the factors for the allowance for credit losses.

The following table details the Company’s nonperforming assets for the periods indicated.

| Consolidated | As of | |||||||||||

| (dollars in thousands; unaudited) | September 30, 2024 | June 30, 2024 | September 30, 2023 | |||||||||

| Nonaccrual loans: | ||||||||||||

| Commercial and industrial loans | $ | 198 | $ | — | $ | 2 | ||||||

| Real estate loans: | ||||||||||||

| Construction, land and land development | — | — | — | |||||||||

| Residential real estate | 44 | 213 | 176 | |||||||||

| Commercial real estate | 831 | 7,731 | 7,145 | |||||||||

| Consumer and other loans: | ||||||||||||

| Credit cards | 7,987 | — | — | |||||||||

| Total nonaccrual loans | 9,060 | 7,944 | 7,323 | |||||||||

| Accruing loans past due 90 days or more: | ||||||||||||

| Commercial & industrial loans | 1,593 | 1,278 | 1,387 | |||||||||

| Real estate loans: | ||||||||||||

| Residential real estate loans | 3,025 | 2,722 | 1,462 | |||||||||

| Consumer and other loans: | ||||||||||||

| Credit cards | 34,562 | 36,465 | 24,807 | |||||||||

| Other consumer and other loans | 6,412 | 4,779 | 8,561 | |||||||||

| Total accruing loans past due 90 days or more | 45,592 | 45,244 | 36,217 | |||||||||

| Total nonperforming loans | 54,652 | 53,188 | 43,540 | |||||||||

| Real estate owned | — | — | — | |||||||||

| Repossessed assets | — | — | — | |||||||||

| Total nonperforming assets | $ | 54,652 | $ | 53,188 | $ | 43,540 | ||||||

| Total nonaccrual loans to loans receivable | 0.27 | % | 0.24 | % | 0.25 | % | ||||||

| Total nonperforming loans to loans receivable | 1.60 | % | 1.60 | % | 1.47 | % | ||||||

| Total nonperforming assets to total assets | 1.34 | % | 1.34 | % | 1.18 | % | ||||||

The following tables detail the CCBX and community bank nonperforming assets which are included in the total nonperforming assets table above.

| CCBX | As of | |||||||||||

| (dollars in thousands; unaudited) | September 30, 2024 | June 30, 2024 | September 30, 2023 | |||||||||

| Nonaccrual loans: | ||||||||||||

| Consumer and other loans: | ||||||||||||

| Credit cards | $ | 7,987 | $ | — | $ | — | ||||||

| Total nonaccrual loans | 7,987 | — | — | |||||||||

| Accruing loans past due 90 days or more: | ||||||||||||

| Commercial & industrial loans | 1,593 | 1,278 | 1,387 | |||||||||

| Real estate loans: | ||||||||||||

| Residential real estate loans | 3,025 | 2,722 | 1,462 | |||||||||

| Consumer and other loans: | ||||||||||||

| Credit cards | 34,562 | 36,465 | 24,807 | |||||||||

| Other consumer and other loans | 6,412 | 4,779 | 8,561 | |||||||||

| Total accruing loans past due 90 days or more | 45,592 | 45,244 | 36,217 | |||||||||

| Total nonperforming loans | 53,579 | 45,244 | 36,217 | |||||||||

| Other real estate owned | — | — | — | |||||||||

| Repossessed assets | — | — | — | |||||||||

| Total nonperforming assets | $ | 53,579 | $ | 45,244 | $ | 36,217 | ||||||

| Total CCBX nonperforming assets to total consolidated assets | 1.32 | % | 1.14 | % | 0.98 | % | ||||||

| Community Bank | As of | |||||||||||

| (dollars in thousands; unaudited) | September 30, 2024 | June 30, 2024 | September 30, 2023 | |||||||||

| Nonaccrual loans: | ||||||||||||

| Commercial and industrial loans | $ | 198 | $ | — | $ | 2 | ||||||

| Real estate: | ||||||||||||

| Construction, land and land development | — | — | — | |||||||||

| Residential real estate | 44 | 213 | 176 | |||||||||

| Commercial real estate | 831 | 7,731 | 7,145 | |||||||||

| Total nonaccrual loans | 1,073 | 7,944 | 7,323 | |||||||||

| Accruing loans past due 90 days or more: | ||||||||||||

| Total accruing loans past due 90 days or more | — | — | — | |||||||||

| Total nonperforming loans | 1,073 | 7,944 | 7,323 | |||||||||

| Other real estate owned | — | — | — | |||||||||

| Repossessed assets | — | — | — | |||||||||

| Total nonperforming assets | $ | 1,073 | $ | 7,944 | $ | 7,323 | ||||||

| Total community bank nonperforming assets to total consolidated assets | 0.03 | % | 0.20 | % | 0.20 | % | ||||||

About Coastal Financial

Coastal Financial Corporation (Nasdaq: CCB) (the “Company”), is an Everett, Washington based bank holding company whose wholly owned subsidiaries are Coastal Community Bank (“Bank”) and Arlington Olympic LLC. The $4.07 billion Bank provides service through 14 branches in Snohomish, Island, and King Counties, the Internet and its mobile banking application. The Bank provides banking as a service to broker-dealers, digital financial service providers, companies and brands that want to provide financial services to their customers through the Bank's CCBX segment. To learn more about the Company visit www.coastalbank.com.

CCB-ER

Contact

Eric Sprink, Chief Executive Officer, (425) 357-3659

Joel Edwards, Executive Vice President & Chief Financial Officer, (425) 357-3687

Forward-Looking Statements

This earnings release contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements reflect our current views with respect to, among other things, future events and our financial performance. Any statements about our management’s expectations, beliefs, plans, predictions, forecasts, objectives, assumptions or future events or performance are not historical facts and may be forward-looking. These statements are often, but not always, made through the use of words or phrases such as “anticipate,” “believes,” “can,” “could,” “may,” “predicts,” “potential,” “should,” “will,” “estimate,” “plans,” “projects,” “continuing,” “ongoing,” “expects,” “intends” and similar words or phrases. Any or all of the forward-looking statements in this earnings release may turn out to be inaccurate. The inclusion of or reference to forward-looking information in this earnings release should not be regarded as a representation by us or any other person that the future plans, estimates or expectations contemplated by us will be achieved. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. Our actual results could differ materially from those anticipated in such forward-looking statements as a result of risks, uncertainties and assumptions that are difficult to predict. Factors that could cause actual results to differ materially from those in the forward-looking statements include, without limitation, the risks and uncertainties discussed under “Risk Factors” in our Annual Report on Form 10-K for the most recent period filed and in any of our subsequent filings with the Securities and Exchange Commission.

If one or more events related to these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may differ materially from what we anticipate. You are cautioned not to place undue reliance on forward-looking statements. Further, any forward-looking statement speaks only as of the date on which it is made, and we undertake no obligation to update or revise any forward-looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events, except as required by law.

| COASTAL FINANCIAL CORPORATION CONDENSED CONSOLIDATED STATEMENTS OF FINANCIAL CONDITION (Dollars in thousands; unaudited) | ||||||||||||||||||||

| ASSETS | ||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | March 31, 2024 | December 31, 2023 | September 30, 2023 | ||||||||||||||||

| Cash and due from banks | $ | 45,327 | $ | 59,995 | $ | 32,790 | $ | 31,345 | $ | 29,984 | ||||||||||

| Interest earning deposits with other banks | 438,699 | 427,250 | 482,338 | 451,783 | 444,962 | |||||||||||||||

| Investment securities, available for sale, at fair value | 38 | 39 | 41 | 99,504 | 98,939 | |||||||||||||||

| Investment securities, held to maturity, at amortized cost | 48,582 | 49,174 | 50,049 | 50,860 | 42,550 | |||||||||||||||

| Other investments | 10,757 | 10,664 | 10,583 | 10,227 | 11,898 | |||||||||||||||

| Loans held for sale | 7,565 | — | 797 | — | — | |||||||||||||||

| Loans receivable | 3,418,832 | 3,326,460 | 3,199,554 | 3,026,092 | 2,967,035 | |||||||||||||||

| Allowance for credit losses | (170,263 | ) | (147,914 | ) | (139,258 | ) | (116,958 | ) | (101,085 | ) | ||||||||||

| Total loans receivable, net | 3,248,569 | 3,178,546 | 3,060,296 | 2,909,134 | 2,865,950 | |||||||||||||||

| CCBX credit enhancement asset | 167,251 | 143,485 | 137,276 | 107,921 | 91,867 | |||||||||||||||

| CCBX receivable | 16,060 | 11,520 | 10,369 | 9,088 | 10,623 | |||||||||||||||

| Premises and equipment, net | 25,833 | 24,526 | 22,995 | 22,090 | 20,543 | |||||||||||||||

| Lease right-of-use assets | 5,427 | 5,635 | 5,756 | 5,932 | 6,126 | |||||||||||||||

| Accrued interest receivable | 23,664 | 23,617 | 24,681 | 26,819 | 23,428 | |||||||||||||||

| Bank-owned life insurance, net | 13,255 | 13,132 | 12,991 | 12,870 | 12,970 | |||||||||||||||

| Deferred tax asset, net | 3,083 | 2,221 | 2,221 | 3,806 | 4,404 | |||||||||||||||

| Other assets | 11,711 | 11,742 | 12,075 | 11,987 | 14,021 | |||||||||||||||

| Total assets | $ | 4,065,821 | $ | 3,961,546 | $ | 3,865,258 | $ | 3,753,366 | $ | 3,678,265 | ||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||||||||||||||

| LIABILITIES | ||||||||||||||||||||

| Deposits | $ | 3,627,288 | $ | 3,543,432 | $ | 3,462,979 | $ | 3,360,363 | $ | 3,289,700 | ||||||||||

| Subordinated debt, net | 44,256 | 44,219 | 44,181 | 44,144 | 44,106 | |||||||||||||||

| Junior subordinated debentures, net | 3,591 | 3,591 | 3,590 | 3,590 | 3,589 | |||||||||||||||

| Deferred compensation | 369 | 405 | 442 | 479 | 513 | |||||||||||||||

| Accrued interest payable | 1,070 | 999 | 1,061 | 892 | 1,056 | |||||||||||||||

| Lease liabilities | 5,609 | 5,821 | 5,946 | 6,124 | 6,321 | |||||||||||||||

| CCBX payable | 39,188 | 34,536 | 33,095 | 33,651 | 38,229 | |||||||||||||||

| Other liabilities | 12,520 | 11,850 | 10,255 | 9,145 | 10,301 | |||||||||||||||

| Total liabilities | 3,733,891 | 3,644,853 | 3,561,549 | 3,458,388 | 3,393,815 | |||||||||||||||

| SHAREHOLDERS’ EQUITY | ||||||||||||||||||||

| Common Stock | 134,769 | 132,989 | 131,601 | 130,136 | 129,244 | |||||||||||||||

| Retained earnings | 197,162 | 183,706 | 172,110 | 165,311 | 156,299 | |||||||||||||||

| Accumulated other comprehensive loss, net of tax | (1 | ) | (2 | ) | (2 | ) | (469 | ) | (1,093 | ) | ||||||||||

| Total shareholders’ equity | 331,930 | 316,693 | 303,709 | 294,978 | 284,450 | |||||||||||||||

| Total liabilities and shareholders’ equity | $ | 4,065,821 | $ | 3,961,546 | $ | 3,865,258 | $ | 3,753,366 | $ | 3,678,265 | ||||||||||

| COASTAL FINANCIAL CORPORATION CONDENSED CONSOLIDATED STATEMENTS OF INCOME (Dollars in thousands, except per share amounts; unaudited) | ||||||||||||||||||

| Three Months Ended | ||||||||||||||||||

| September 30, 2024 | June 30, 2024 | March 31, 2024 | December 31, 2023 | September 30, 2023 | ||||||||||||||

| INTEREST AND DIVIDEND INCOME | ||||||||||||||||||

| Interest and fees on loans | $ | 99,590 | $ | 90,944 | $ | 84,621 | $ | 81,159 | $ | 83,652 | ||||||||

| Interest on interest earning deposits with other banks | 4,781 | 5,683 | 4,780 | 5,687 | 3,884 | |||||||||||||

| Interest on investment securities | 675 | 686 | 1,034 | 1,225 | 766 | |||||||||||||

| Dividends on other investments | 33 | 174 | 37 | 172 | 29 | |||||||||||||

| Total interest income | 105,079 | 97,487 | 90,472 | 88,243 | 88,331 | |||||||||||||

| INTEREST EXPENSE | ||||||||||||||||||

| Interest on deposits | 32,083 | 30,578 | 28,867 | 27,916 | 25,451 | |||||||||||||

| Interest on borrowed funds | 809 | 672 | 669 | 670 | 651 | |||||||||||||

| Total interest expense | 32,892 | 31,250 | 29,536 | 28,586 | 26,102 | |||||||||||||

| Net interest income | 72,187 | 66,237 | 60,936 | 59,657 | 62,229 | |||||||||||||

| PROVISION FOR CREDIT LOSSES | 70,257 | 62,325 | 83,158 | 60,789 | 27,253 | |||||||||||||

| Net interest income/(expense) after provision for credit losses | 1,930 | 3,912 | (22,222 | ) | (1,132 | ) | 34,976 | |||||||||||

| NONINTEREST INCOME | ||||||||||||||||||

| Deposit service charges and fees | 952 | 946 | 908 | 957 | 998 | |||||||||||||

| Loan referral fees | — | — | 168 | — | 1 | |||||||||||||

| Gain on sales of loans, net | — | — | — | — | 107 | |||||||||||||

| Unrealized gain (loss) on equity securities, net | 2 | 9 | 15 | 80 | 5 | |||||||||||||

| Other income | 486 | 257 | 308 | 60 | 291 | |||||||||||||

| Noninterest income, excluding BaaS program income and BaaS indemnification income | 1,440 | 1,212 | 1,399 | 1,097 | 1,402 | |||||||||||||

| Servicing and other BaaS fees | 1,044 | 1,525 | 1,131 | 1,015 | 997 | |||||||||||||

| Transaction fees | 1,696 | 1,309 | 1,122 | 1,006 | 1,036 | |||||||||||||

| Interchange fees | 1,853 | 1,625 | 1,539 | 1,272 | 1,216 | |||||||||||||

| Reimbursement of expenses | 1,843 | 1,637 | 1,033 | 1,076 | 1,152 | |||||||||||||

| BaaS program income | 6,436 | 6,096 | 4,825 | 4,369 | 4,401 | |||||||||||||

| BaaS credit enhancements | 70,108 | 60,826 | 79,808 | 58,449 | 25,926 | |||||||||||||

| BaaS fraud enhancements | 2,084 | 1,784 | 923 | 779 | 2,850 | |||||||||||||

| BaaS indemnification income | 72,192 | 62,610 | 80,731 | 59,228 | 28,776 | |||||||||||||

| Total noninterest income | 80,068 | 69,918 | 86,955 | 64,694 | 34,579 | |||||||||||||

| NONINTEREST EXPENSE | ||||||||||||||||||

| Salaries and employee benefits | 17,101 | 17,005 | 17,984 | 16,490 | 18,087 | |||||||||||||

| Occupancy | 1,750 | 1,686 | 1,518 | 1,340 | 1,224 | |||||||||||||

| Data processing and software licenses | 3,511 | 2,924 | 2,892 | 2,417 | 2,366 | |||||||||||||

| Legal and professional expenses | 3,597 | 3,631 | 3,672 | 2,649 | 4,447 | |||||||||||||

| Point of sale expense | 1,351 | 852 | 869 | 899 | 1,068 | |||||||||||||

| Excise taxes | 762 | (706 | ) | 320 | 449 | 541 | ||||||||||||

| Federal Deposit Insurance Corporation ("FDIC") assessments | 740 | 690 | 683 | 665 | 694 | |||||||||||||

| Director and staff expenses | 559 | 470 | 400 | 478 | 529 | |||||||||||||

| Marketing | 67 | 14 | 53 | 138 | 169 | |||||||||||||

| Other expense | 1,482 | 1,383 | 1,867 | 1,089 | 1,523 | |||||||||||||

| Noninterest expense, excluding BaaS loan and BaaS fraud expense | 30,920 | 27,949 | 30,258 | 26,614 | 30,648 | |||||||||||||

| BaaS loan expense | 32,612 | 29,076 | 24,837 | 24,310 | 23,003 | |||||||||||||

| BaaS fraud expense | 2,084 | 1,784 | 923 | 779 | 2,850 | |||||||||||||

| BaaS loan and fraud expense | 34,696 | 30,860 | 25,760 | 25,089 | 25,853 | |||||||||||||

| Total noninterest expense | 65,616 | 58,809 | 56,018 | 51,703 | 56,501 | |||||||||||||

| Income before provision for income taxes | 16,382 | 15,021 | 8,715 | 11,859 | 13,054 | |||||||||||||

| PROVISION FOR INCOME TAXES | 2,926 | 3,425 | 1,915 | 2,847 | 2,784 | |||||||||||||

| NET INCOME | $ | 13,456 | $ | 11,596 | $ | 6,800 | $ | 9,012 | $ | 10,270 | ||||||||

| Basic earnings per common share | $ | 1.00 | $ | 0.86 | $ | 0.51 | $ | 0.68 | $ | 0.77 | ||||||||

| Diluted earnings per common share | $ | 0.97 | $ | 0.84 | $ | 0.50 | $ | 0.66 | $ | 0.75 | ||||||||

| Weighted average number of common shares outstanding: | ||||||||||||||||||

| Basic | 13,447,066 | 13,412,667 | 13,340,997 | 13,286,828 | 13,285,974 | |||||||||||||

| Diluted | 13,822,270 | 13,736,508 | 13,676,917 | 13,676,513 | 13,675,833 | |||||||||||||

| COASTAL FINANCIAL CORPORATION AVERAGE BALANCES, YIELDS, AND RATES – QUARTERLY (Dollars in thousands; unaudited) | ||||||||||||||||||||||||||||||

| For the Three Months Ended | ||||||||||||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | September 30, 2023 | ||||||||||||||||||||||||||||

| Average Balance | Interest & Dividends | Yield / Cost (1) | Average Balance | Interest & Dividends | Yield / Cost (1) | Average Balance | Interest & Dividends | Yield / Cost (1) | ||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||||||||

| Interest earning assets: | ||||||||||||||||||||||||||||||

| Interest earning deposits with other banks | $ | 350,915 | $ | 4,781 | 5.42 | % | $ | 418,165 | $ | 5,683 | 5.47 | % | $ | 285,596 | $ | 3,884 | 5.40 | % | ||||||||||||

| Investment securities, available for sale (2) | 40 | — | — | 43 | — | 3.13 | 100,283 | 543 | 2.15 | |||||||||||||||||||||

| Investment securities, held to maturity (2) | 48,945 | 675 | 5.49 | 49,737 | 686 | 5.55 | 17,703 | 223 | 5.00 | |||||||||||||||||||||

| Other investments | 11,140 | 33 | 1.18 | 10,592 | 174 | 6.61 | 11,943 | 29 | 0.96 | |||||||||||||||||||||

| Loans receivable (3) | 3,464,871 | 99,590 | 11.43 | 3,258,042 | 90,944 | 11.23 | 3,062,214 | 83,652 | 10.84 | |||||||||||||||||||||

| Total interest earning assets | 3,875,911 | 105,079 | 10.79 | 3,736,579 | 97,487 | 10.49 | 3,477,739 | 88,331 | 10.08 | |||||||||||||||||||||

| Noninterest earning assets: | ||||||||||||||||||||||||||||||

| Allowance for credit losses | (151,292 | ) | (138,472 | ) | (100,329 | ) | ||||||||||||||||||||||||

| Other noninterest earning assets | 268,903 | 255,205 | 220,750 | |||||||||||||||||||||||||||

| Total assets | $ | 3,993,522 | $ | 3,853,312 | $ | 3,598,160 | ||||||||||||||||||||||||

| Liabilities and Shareholders’ Equity | ||||||||||||||||||||||||||||||

| Interest bearing liabilities: | ||||||||||||||||||||||||||||||

| Interest bearing deposits | $ | 2,966,527 | $ | 32,083 | 4.30 | % | $ | 2,854,575 | $ | 30,578 | 4.31 | % | $ | 2,515,093 | $ | 25,451 | 4.01 | % | ||||||||||||

| FHLB advances and other borrowings | 9,717 | 140 | 5.73 | 1,648 | 3 | 0.73 | — | — | — | |||||||||||||||||||||

| Subordinated debt | 44,234 | 598 | 5.38 | 44,197 | 598 | 5.44 | 44,084 | 580 | 5.22 | |||||||||||||||||||||

| Junior subordinated debentures | 3,591 | 71 | 7.87 | 3,590 | 71 | 7.95 | 3,589 | 71 | 7.85 | |||||||||||||||||||||

| Total interest bearing liabilities | 3,024,069 | 32,892 | 4.33 | 2,904,010 | 31,250 | 4.33 | 2,562,766 | 26,102 | 4.04 | |||||||||||||||||||||

| Noninterest bearing deposits | 588,178 | 584,661 | 698,532 | |||||||||||||||||||||||||||

| Other liabilities | 60,101 | 58,267 | 57,865 | |||||||||||||||||||||||||||

| Total shareholders' equity | 321,174 | 306,374 | 278,997 | |||||||||||||||||||||||||||

| Total liabilities and shareholders' equity | $ | 3,993,522 | $ | 3,853,312 | $ | 3,598,160 | ||||||||||||||||||||||||

| Net interest income | $ | 72,187 | $ | 66,237 | $ | 62,229 | ||||||||||||||||||||||||

| Interest rate spread | 6.46 | % | 6.17 | % | 6.04 | % | ||||||||||||||||||||||||

| Net interest margin (4) | 7.41 | % | 7.13 | % | 7.10 | % | ||||||||||||||||||||||||

(1) Yields and costs are annualized.

(2) For presentation in this table, average balances and the corresponding average rates for investment securities are based upon historical cost, adjusted for amortization of premiums and accretion of discounts.

(3) Includes loans held for sale and nonaccrual loans.

(4) Net interest margin represents net interest income divided by the average total interest earning assets.

| COASTAL FINANCIAL CORPORATION SELECTED AVERAGE BALANCES, YIELDS, AND RATES – BY SEGMENT - QUARTERLY (Dollars in thousands; unaudited) | |||||||||||||||||||||||||||

| For the Three Months Ended | |||||||||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | September 30, 2023 | |||||||||||||||||||||||||

| (dollars in thousands, unaudited) | Average Balance | Interest & Dividends | Yield / Cost (1) | Average Balance | Interest & Dividends | Yield / Cost (1) | Average Balance | Interest & Dividends | Yield / Cost (1) | ||||||||||||||||||

| Community Bank | |||||||||||||||||||||||||||

| Assets | |||||||||||||||||||||||||||

| Interest earning assets: | |||||||||||||||||||||||||||

| Loans receivable (2) | $ | 1,912,428 | $ | 31,898 | 6.64 | % | $ | 1,895,699 | $ | 30,741 | 6.52 | % | $ | 1,752,834 | $ | 27,373 | 6.20 | % | |||||||||

| Total interest earning assets | 1,912,428 | 31,898 | 6.64 | 1,895,699 | 30,741 | 6.52 | 1,752,834 | 27,373 | 6.20 | ||||||||||||||||||

| Liabilities | |||||||||||||||||||||||||||

| Interest bearing liabilities: | |||||||||||||||||||||||||||

| Interest bearing deposits | 982,280 | 7,264 | 2.94 | % | 938,033 | 6,459 | 2.77 | % | 920,707 | 5,067 | 2.18 | % | |||||||||||||||

| Intrabank liability | 406,641 | 5,540 | 5.42 | 429,452 | 5,836 | 5.47 | 223,221 | 3,036 | 5.40 | ||||||||||||||||||

| Total interest bearing liabilities | 1,388,921 | 12,804 | 3.67 | 1,367,485 | 12,295 | 3.62 | 1,143,928 | 8,103 | 2.81 | ||||||||||||||||||

| Noninterest bearing deposits | 523,507 | 528,214 | 608,906 | ||||||||||||||||||||||||

| Net interest income | $ | 19,094 | $ | 18,446 | $ | 19,270 | |||||||||||||||||||||

| Net interest margin(3) | 3.97 | % | 3.91 | % | 4.36 | % | |||||||||||||||||||||

| CCBX | |||||||||||||||||||||||||||

| Assets | |||||||||||||||||||||||||||

| Interest earning assets: | |||||||||||||||||||||||||||

| Loans receivable (2)(4) | $ | 1,552,443 | $ | 67,692 | 17.35 | % | $ | 1,362,343 | $ | 60,203 | 17.77 | % | $ | 1,309,380 | $ | 56,279 | 17.05 | % | |||||||||

| Intrabank asset | 496,475 | 6,764 | 5.42 | 610,646 | 8,299 | 5.47 | 374,632 | 5,095 | 5.40 | ||||||||||||||||||

| Total interest earning assets | 2,048,918 | 74,456 | 14.46 | 1,972,989 | 68,502 | 13.96 | 1,684,012 | 61,374 | 14.46 | ||||||||||||||||||

| Liabilities | |||||||||||||||||||||||||||

| Interest bearing liabilities: | |||||||||||||||||||||||||||

| Interest bearing deposits | 1,984,247 | 24,819 | 4.98 | % | 1,916,542 | 24,119 | 5.06 | % | 1,594,386 | 20,384 | 5.07 | % | |||||||||||||||

| Total interest bearing liabilities | 1,984,247 | 24,819 | 4.98 | 1,916,542 | 24,119 | 5.06 | 1,594,386 | 20,384 | 5.07 | ||||||||||||||||||

| Noninterest bearing deposits | 64,671 | 56,447 | 89,626 | ||||||||||||||||||||||||

| Net interest income | $ | 49,637 | $ | 44,383 | $ | 40,990 | |||||||||||||||||||||

| Net interest margin(3) | 9.64 | % | 9.05 | % | 9.66 | % | |||||||||||||||||||||

| Net interest margin, net of Baas loan expense (5) | 3.31 | % | 3.12 | % | 4.24 | % | |||||||||||||||||||||

| For the Three Months Ended | |||||||||||||||||||||||||||

| September 30, 2024 | June 30, 2024 | September 30, 2023 | |||||||||||||||||||||||||

| (dollars in thousands, unaudited) | Average Balance | Interest & Dividends | Yield / Cost (1) | Average Balance | Interest & Dividends | Yield / Cost (1) | Average Balance | Interest & Dividends | Yield / Cost (1) | ||||||||||||||||||

| Treasury & Administration | |||||||||||||||||||||||||||

| Assets | |||||||||||||||||||||||||||

| Interest earning assets: | |||||||||||||||||||||||||||

| Interest earning deposits with other banks | $ | 350,915 | $ | 4,781 | 5.42 | % | $ | 418,165 | $ | 5,683 | 5.47 | % | $ | 285,596 | $ | 3,884 | 5.40 | % | |||||||||

| Investment securities, available for sale (6) | 40 | — | — | 43 | — | 3.13 | 100,283 | 543 | 2.15 | ||||||||||||||||||

| Investment securities, held to maturity (6) | 48,945 | 675 | 5.49 | 49,737 | 686 | 5.55 | 17,703 | 223 | 5.00 | ||||||||||||||||||

| Other investments | 11,140 | 33 | 1.18 | 10,592 | 174 | 6.61 | 11,943 | 29 | 0.96 | ||||||||||||||||||

| Total interest earning assets | 411,040 | 5,489 | 5.31 | % | 478,537 | 6,543 | 5.50 | % | 415,525 | 4,679 | 4.47 | % | |||||||||||||||

| Liabilities | |||||||||||||||||||||||||||

| Interest bearing liabilities: | |||||||||||||||||||||||||||

| FHLB advances and borrowings | $ | 9,717 | $ | 140 | 5.73 | % | 1,648 | 3 | 0.73 | % | — | — | — | % | |||||||||||||

| Subordinated debt | 44,234 | 598 | 5.38 | % | 44,197 | 598 | 5.44 | % | 44,084 | 580 | 5.22 | % | |||||||||||||||

| Junior subordinated debentures | 3,591 | 71 | 7.87 | 3,590 | 71 | 7.95 | 3,589 | 71 | 7.85 | ||||||||||||||||||

| Intrabank liability, net (7) | 89,834 | 1,224 | 5.42 | 181,194 | 2,463 | 5.47 | 151,411 | 2,059 | 5.40 | ||||||||||||||||||

| Total interest bearing liabilities | 147,376 | 2,033 | 5.49 | 230,629 | 3,135 | 5.47 | 199,084 | 2,710 | 5.40 | ||||||||||||||||||

| Net interest income | $ | 3,456 | $ | 3,408 | $ | 1,969 | |||||||||||||||||||||

| Net interest margin(3) | 3.34 | % | 2.86 | % | 1.88 | % | |||||||||||||||||||||

(1) Yields and costs are annualized.

(2) Includes loans held for sale and nonaccrual loans.

(3) Net interest margin represents net interest income divided by the average total interest earning assets.

(4) CCBX yield does not include the impact of BaaS loan expense. BaaS loan expense represents the amount paid or payable to partners for credit enhancements, fraud enhancements and originating & servicing CCBX loans. See reconciliation of the non-GAAP measures at the end of this earnings release for the impact of BaaS loan expense on CCBX loan yield.

(5) Net interest margin, net of BaaS loan expense includes the impact of BaaS loan expense. BaaS loan expense represents the amount paid or payable to partners for credit enhancements, fraud enhancements, originating & servicing CCBX loans. See reconciliation of the non-GAAP measures at the end of this earnings release.

(6) For presentation in this table, average balances and the corresponding average rates for investment securities are based upon historical cost, adjusted for amortization of premiums and accretion of discounts.

(7) Intrabank assets and liabilities are consolidated for period calculations and presented as intrabank asset, net or intrabank liability, net in the table above.

Non-GAAP Financial Measures

The Company uses certain non-GAAP financial measures to provide meaningful supplemental information regarding the Company’s operational performance and to enhance investors’ overall understanding of such financial performance.

However, these non-GAAP financial measures are supplemental and are not a substitute for an analysis based on GAAP measures. As other companies may use different calculations for these adjusted measures, this presentation may not be comparable to other similarly titled adjusted measures reported by other companies.

The following non-GAAP measures are presented to illustrate the impact of BaaS loan expense on net loan income and yield on CCBX loans and the impact of BaaS loan expense on net interest income and net interest margin.

Net BaaS loan income divided by average CCBX loans is a non-GAAP measure that includes the impact BaaS loan expense on net BaaS loan income and the yield on CCBX loans. The most directly comparable GAAP measure is yield on CCBX loans.

Net interest income net of BaaS loan expense is a non-GAAP measure that includes the impact BaaS loan expense on net interest income. The most directly comparable GAAP measure is net interest income.

Net interest margin, net of BaaS loan expense is a non-GAAP measure that includes the impact of BaaS loan expense on net interest rate margin. The most directly comparable GAAP measure is net interest margin.

Reconciliations of the GAAP and non-GAAP measures are presented below.

| As of and for the Three Months Ended | ||||||||||||

| (dollars in thousands; unaudited) | September 30, 2024 | June 30, 2024 | September 30, 2023 | |||||||||

| Net BaaS loan income divided by average CCBX loans: | ||||||||||||

| CCBX loan yield (GAAP)(1) | 17.35 | % | 17.77 | % | 17.05 | % | ||||||

| Total average CCBX loans receivable | $ | 1,552,443 | $ | 1,362,343 | $ | 1,309,380 | ||||||

| Interest and earned fee income on CCBX loans (GAAP) | 67,692 | 60,203 | 56,279 | |||||||||

| BaaS loan expense | (32,612 | ) | (29,076 | ) | (23,003 | ) | ||||||

| Net BaaS loan income | $ | 35,080 | $ | 31,127 | $ | 33,276 | ||||||

| Net BaaS loan income divided by average CCBX loans (1) | 8.99 | % | 9.19 | % | 10.08 | % | ||||||

| Net interest margin, net of BaaS loan expense: | ||||||||||||

| CCBX interest margin (1) | 9.64 | % | 9.05 | % | 9.66 | % | ||||||

| CCBX earning assets | 2,048,918 | 1,972,989 | 1,684,012 | |||||||||

| Net interest income | 49,637 | 44,383 | 40,990 | |||||||||

| Less: BaaS loan expense | (32,612 | ) | (29,076 | ) | (23,003 | ) | ||||||

| Net interest income, net of BaaS loan expense | $ | 17,025 | $ | 15,307 | $ | 17,987 | ||||||

| CCBX net interest margin, net of BaaS loan expense (1) | 3.31 | % | 3.12 | % | 4.24 | % | ||||||

(1) Annualized calculations for periods presented.

APPENDIX A -

As of September 30, 2024

Industry Concentration

We have a diversified loan portfolio, representing a wide variety of industries. Our major categories of loans are commercial real estate, consumer and other loans, residential real estate, commercial and industrial, and construction, land and land development loans. Together they represent $3.43 billion in outstanding loan balances. When combined with $2.29 billion in unused commitments the total of these categories is $5.72 billion.

Commercial real estate loans represent the largest segment of our loans, comprising 39.8% of our total balance of outstanding loans as of September 30, 2024. Unused commitments to extend credit represents an additional $41.5 million, and the combined total in commercial real estate loans represents $1.40 billion, or 24.6% of our total outstanding loans and loan commitments.

The following table summarizes our loan commitment by industry for our commercial real estate portfolio as of September 30, 2024:

| (dollars in thousands; unaudited) | Outstanding Balance | Available Loan Commitments | Total Outstanding Balance & Available Commitment | % of Total Loans (Outstanding Balance & Available Commitment) | Average Loan Balance | Number of Loans | |||||||||||

| Apartments | $ | 382,498 | $ | 5,685 | $ | 388,183 | 6.8 | % | $ | 3,714 | 103 | ||||||

| Hotel/Motel | 155,441 | 189 | 155,630 | 2.7 | 6,758 | 23 | |||||||||||

| Convenience Store | 142,366 | 614 | 142,980 | 2.5 | 2,296 | 62 | |||||||||||

| Office | 123,423 | 8,204 | 131,627 | 2.3 | 1,371 | 90 | |||||||||||

| Warehouse | 102,818 | 2,000 | 104,818 | 1.8 | 1,743 | 59 | |||||||||||

| Retail | 107,934 | 620 | 108,554 | 1.9 | 1,018 | 106 | |||||||||||

| Mixed use | 93,490 | 5,273 | 98,763 | 1.7 | 1,154 | 81 | |||||||||||

| Mini Storage | 79,395 | 14,330 | 93,725 | 1.7 | 3,452 | 23 | |||||||||||

| Strip Mall | 44,089 | — | 44,089 | 0.8 | 6,298 | 7 | |||||||||||

| Manufacturing | 34,599 | 1,200 | 35,799 | 0.6 | 1,193 | 29 | |||||||||||

| Groups < 0.70% of total | 96,393 | 3,392 | 99,785 | 1.8 | 1,205 | 80 | |||||||||||

| Total | $ | 1,362,446 | $ | 41,507 | $ | 1,403,953 | 24.6 | % | $ | 2,055 | 663 | ||||||

Consumer loans comprise 33.0% of our total balance of outstanding loans as of September 30, 2024. Unused commitments to extend credit represents an additional $1.07 billion, and the combined total in consumer and other loans represents $2.20 billion, or 38.4% of our total outstanding loans and loan commitments. As illustrated in the table below, our CCBX partners bring in a large number of mostly smaller dollar loans, resulting in an average consumer loan balance of just $900. CCBX consumer loans are underwritten to CCBX credit standards and underwriting of these loans is regularly tested, including quarterly testing for partners with portfolio balances greater than $10.0 million.

The following table summarizes our loan commitment by industry for our consumer and other loan portfolio as of September 30, 2024:

| (dollars in thousands; unaudited) | Outstanding Balance | Available Loan Commitments | Total Outstanding Balance & Available Commitment (1) | % of Total Loans (Outstanding Balance & Available Commitment) | Average Loan Balance | Number of Loans | |||||||||||

| CCBX consumer loans | |||||||||||||||||

| Credit cards | $ | 633,691 | $ | 1,055,684 | $ | 1,689,375 | 29.5 | % | $ | 1.7 | 369,404 | ||||||

| Installment loans | 471,813 | 7,112 | 478,925 | 8.4 | 0.9 | 513,897 | |||||||||||

| Lines of credit | 1,362 | — | 1,362 | 0.0 | 2.4 | 558 | |||||||||||

| Other loans | 9,053 | — | 9,053 | 0.2 | — | 365,834 | |||||||||||

| Community bank consumer loans | |||||||||||||||||

| Installment loans | 1,291 | 1 | 1,292 | 0.0 | 51.6 | 25 | |||||||||||

| Lines of credit | 194 | 365 | 559 | 0.0 | 6.1 | 32 | |||||||||||

| Other loans | 12,688 | 3,000 | 15,688 | 0.3 | 32.5 | 390 | |||||||||||

| Total | $ | 1,130,092 | $ | 1,066,162 | $ | 2,196,254 | 38.4 | % | $ | 0.9 | 1,250,140 | ||||||